Advanced Equity Structuring for Tax and Control Optimization

In this article, we will discuss four such advanced equity structuring techniques and tax minimization strategies.

In the USA, due to double taxation, as much as 50.23% of the income generated by an investor could be captured by taxes. However, through strategies such as QSBS investing, adoption of pass-through entity structure, and informed deal structuring, private equity investors can unlock significant tax savings.

Similarly, adopting the right equity structure allows entrepreneurs to maintain control while addressing investor needs.

Effective equity structuring strategies

Designing an effective equity structure is critical for startups, acquisitions, and established companies seeking to align incentives, retain control, attract investment, and motivate key stakeholders. Below are proven strategies and best practices supported by recent insights.

Entity and Equity Structure Selection

In the USA, investors are subject to double taxation; first at the corporate level and then at the individual level. One way to bypass double taxation is to invest in companies structured as pass-through entities.

Partnerships and small business corporations (S-corporations) are pass-through entities wherein any profits or losses are passed through without taxation to the shareholders. Since partnerships expose investors to unlimited liability and inhibit fundraising ability, an S-corporation is the appropriate business structure in private equity.

You can also adopt hybrid and multi-jurisdictional entities and equity structures to optimize tax impact and control over your business. For instance, at Facebook, Mark Zuckerberg enforced a dual-class share structure to ensure control over his company. Also, many startups incorporate in Delaware to take advantage of business-friendly corporate law and taxation policies.

Deal Structuring for Tax Efficiency

Certain types of mergers and acquisitions (M&As) that qualify for tax-free treatment as per the Internal Revenue Code (IRC) are as follows:

| IRC Section | Transaction type | Key requirements for tax-free treatment |

|---|---|---|

| 368(a)(1)(A) | Statutory merger | |

| 368(a)(1)(B) | 100% stock acquisition | |

| 368(a)(1)(C) | Practical merger | |

| 368(a)(1)(D) | Acquisitive transactions | |

| 355 | Spin-offs, split-offs, and split-ups |

Control Optimization within Equity Structures

Most venture capital firms and angel investors manage a portfolio of about 20 startups and do not wish to be involved in the day-to-day operations of their portfolio companies. So, such investors are likely to provide funding even in exchange for non-voting equity.

An investor who would like to periodically recover a part of their investment basis might rather receive preferred stock than common stock. Some investors may be willing to waive their voting rights in exchange for favorable waterfall arrangements. This simply means that payouts to these investors would be given higher priority than other stakeholders in the event of acquisitions, dissolutions, mergers, IPOs, and other exit events.

Another source of control dilution could be stock-based compensation, a widely used tool for employee retention and attracting talent. When you issue common stock options as compensation to employees, you can expect a constant rate of dilution. If you increase the size of your workforce, the dilution rate would accelerate.

Even then, such dilution may seem marginal. However, the combined ownership of employees might eventually add up to a substantial voting influence. To avoid such scenarios, you should consider stock-based compensation such as phantom stocks and stock appreciation rights (SARs).

Tax Optimization Across the Investment Lifecycle

By investing through qualified small business stock (QSBS), private equity investors can exclude gains up to $10 million or 10 times their investment basis, whichever is higher. A key requirement to qualify for these tax benefits is that the business must have gross assets worth up to $50 million, with at least 80% of these assets being engaged in qualified businesses.

During the investment period, private equity investors should also educate entrepreneurs about tax optimization practices such as research and development (R&D) tax credit and writing off certain assets in the purchase year itself.

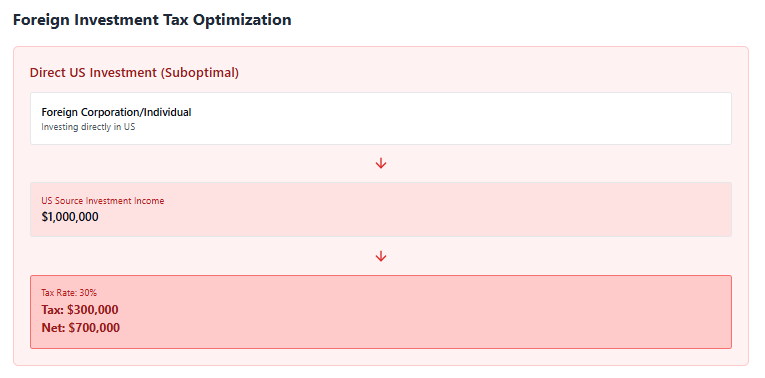

Furthermore, foreign individuals and corporations investing in the USA are typically subjected to a 30% tax rate on US-source investment income. However, this rate can be reduced to 21% by taking two strategic steps.

First, incorporate an investment company in the Commonwealth of the Northern Mariana Islands (CNMI). Such corporations are not treated as foreign corporations under Section 1442 and are therefore exempt from the 30% tax. These corporations are subject to a 21% tax paid to the CNMI government.

Secondly, your corporation must avoid engaging a USToB (US trade or business) as that would trigger a tax of 30% on the investment.

Eqvista – Accurate valuations for agile decision-making!

Currently, the private equity market is facing a lack of liquidity. According to Bain & Company, 63% of limited partners are willing to accept a conventional buyout even if it is at a valuation below recent marks. In such circumstances, investors must act with agility to avoid missing out on exit opportunities.

Eqvista’s valuation software allows you to compare buyout offers with real-time valuation updates. This can help you avoid giving an undue discount. Contact us to get a demonstration!

Interested in issuing & managing shares?

If you want to start issuing and managing shares, Try out our Eqvista App, it is free and all online!