According to the Hurun Global Unicorn Index, 128 unicorn valuations dropped in 2023. Of these 128 unicorn companies, 42 lost their unicorn status. Half of the companies that lost their unicorn status were American. This trend has sparked fears of the overvaluation of unicorn companies, especially in the USA.

Many investors are now questioning the sustainability of unicorn companies. In order to avoid making the same mistakes as 2021, it has become extremely important to understand the dynamics between startup valuations and macroeconomic conditions.

Hence, in this article, we will explore how low interest rates may have artificially propped up startup valuations in 2021 and why we may see a repeat of the same trend. Additionally, we explore the rise of ZIRPicorns and papercorns and identify industries most vulnerable to valuation bubbles.

Is cheap debt inflating unicorn valuations?

When interest rates fall, business valuations increase because of three reasons. Firstly, this reduces the propensity to save and encourages consumption.

Secondly, lower interest rates mean cheap access to credit.

Thirdly, and most importantly, it magnifies the ability of investors to take on debt for financing startups.

Many suspect that the third reason might be the primary cause of over-inflated startup valuations. After all, this is a phenomenon we have observed quite recently.In order to stimulate the economy, central banks all over the world drastically reduced interest rates when the COVID-19 pandemic started.

From March 2020 to 2022, the US Federal Reserve maintained the federal funds interest rate at 0.25%. A direct result of the low interest rates was a sharp uptick in housing prices in 2021. From May 2020 to May 2021, the US FHFA House Price Index rose sharply by 17.99%. In comparison, this index rose by only 5.12% from May 2019 to May 2020.

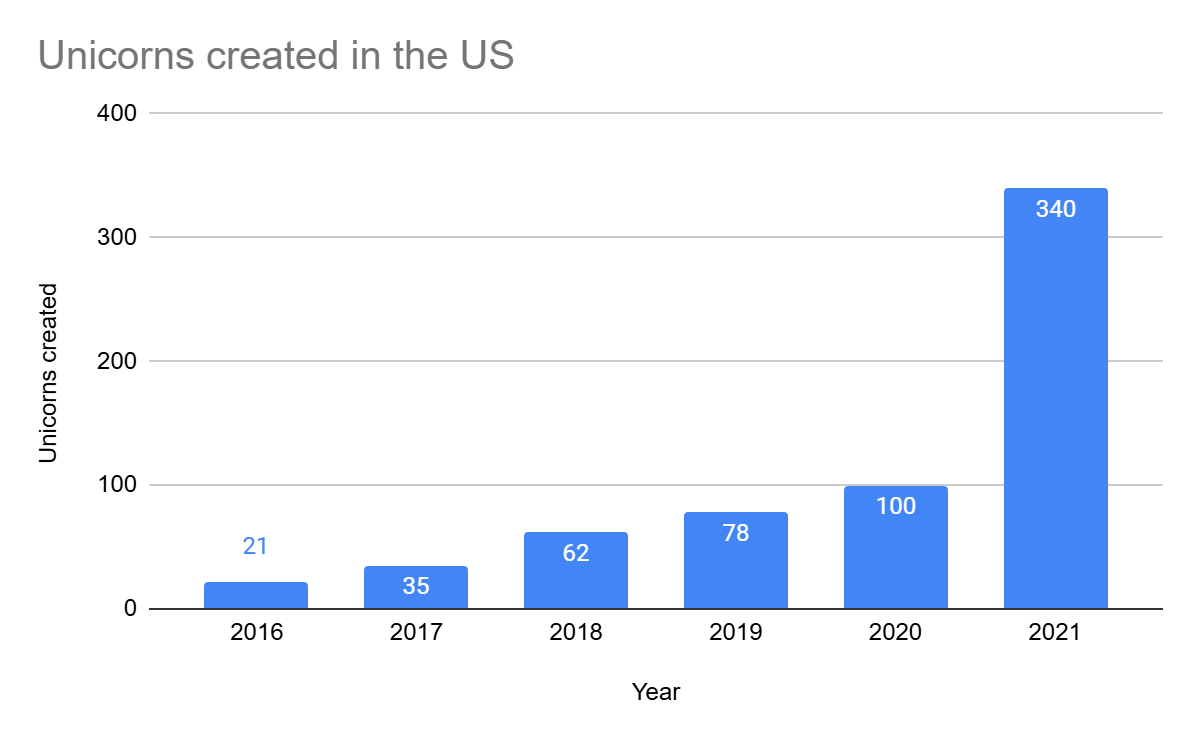

Another important piece of evidence for low interest rates causing increased investment activity is the fact that more unicorns were created in 2021 than in the previous five years combined.

Source: Pitchbook

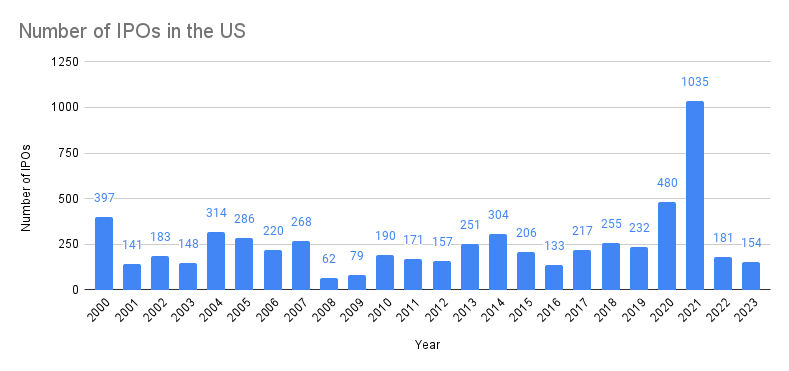

Our theory is also validated by the fact that the number of initial public offerings (IPOs) in 2021 was more than double that of IPOs in 2020.

As the interest rates rose in the US, the funding to US startups dried up. In 2022, funds raised by US startups fell by 29.8% to $242.2 billion and in 2023, the funding dropped by 29.56% to $170.6 billion.

This brings us to the current dilemma. A record number of companies lost their unicorn status in 2023. Post this massive correction, the US Federal Reserve has cut interest rates by 1%, and 2 additional rate cuts are projected in 2025. Hence, many fear that cheap money may reinflate speculative bubbles across asset classes, especially in unicorn companies.

Rise of the ZIRPicorns and papercorns!

Billion-dollar startups were first termed as unicorns by Aileen Lee in 2013. In 2024, Lee introduced a new intriguing term, ZIRPicorns.

Note: ZIRPicorns refers to startups that achieved unicorn status during the zero-interest-rate period (ZIRP) of 2021 but have not closed any funding rounds since then.

At the start of 2024, Lee claimed that 60% of American unicorns were ZIRPicorns.Another striking claim made by Lee was that 93% of unicorns were papercorns.

Note: Papercorns are companies that are privately valued as unicorns on paper but have not provided any meaningful exits.

According to Lee, 40% of the unicorns were trading at valuations lower than $1 billion in the secondary market. Given the current liquidity levels and investor sentiment in the private equity market, we cannot discount Lee’s claims as pure conjecture.

According to CB Insights, of the more than 1,200 startups in the world, more than 33% have not raised funds since the low-interest period of 2021. But what happens when a 2021 unicorn raises money in 2024? To answer this, we need not look any further than TrueLayer.

TrueLayer is a startup that enables real-time bank payments across the UK and Europe, a service widely used by players in the industries of financial services, i-gaming, e-commerce, travel, and crypto. It also enables businesses, especially the ones in the financial services industry, to retrieve transaction and identity data to onboard clients. Given the wide-ranging application and scalability of their solutions, TrueLayer achieved a valuation of $1 billion in a 2021 funding round.

However, in 2024, in the extension of the same funding round, the company’s valuation dropped by 30% to $700 million. TrueLayer experienced this valuation drop despite tripling its revenue to £12.4 million in 2023 compared to the previous year, driven by the increased adoption of its platform.

Industries facing the greatest bubble risks

Some of the industries that might be facing the greatest bubble risks are as follows:

Artificial intelligence (AI)

Of late, AI startups have been achieving exuberant valuations, some of which may not be justifiable. For instance, Safe Superintelligence was founded in June 2024 and in September, the company raised $1 billion at a $5 billion valuation in its seed funding round.

While the startup is headed by Sutskever, OpenAI’s former chief scientist, and is chasing a lucrative vision of developing AI that does not harm humans, the company was still only three months old when it reached the $5 billion valuation.

Spacetech

Although overshadowed by AI, the space tech industry has been picking up in recent years. A recent tender offer valued SpaceX at $350 billion making it the most valuable startup in the world. Other unicorns in this industry include Sierra Space, Relativity Space, ABL Space Systems, Firefly Aerospace, Axiom Space, and GalaxySpace.

However, many believe that investor enthusiasm in this sector may be premature since the business models in this industry suffer from unproven revenue models, high research and development (R&D) costs, and testing challenges.

Fintech

Fintech startups, especially the ones working in the lending and related sectors, may experience inflated valuations as the US Federal Reserve reduces interest rates. This would directly, albeit temporarily, improve the net interest margin for many fintech startups, thus presenting a rose-tinted view of performance to prospective investors.

Another factor that can over-inflate the value of fintech companies is the fact that as economic activity picks up as a result of low interest rates, and transaction values and volumes rise, fintech companies are well-positioned to experience revenue growth.

The US economy has just recovered from a period of high inflation. Hence, it is entirely possible for the US Federal Reserve to go back on its interest rate easing stance and thereby trigger a reversal in fintech growth trends.

Eqvista- Empowering Smarter Choices!

The close-to-zero interest rate period of 2020-22 caused spikes in asset prices across the board and startup valuations were no exceptions. In 2021, a record number of startups attained unicorn status, however, this trend was reversed the very next year.

A similar phenomenon can be observed in public listings with the number of IPOs spiking in 2021 but falling back sharply in 2022. The emergence of ZIRPicorns and papercorns also corroborates the unsustainability of startup valuations achieved in 2021. As the US Federal Reserve reduces interest rates, we may, once again, see overinflation of startup valuations, especially in the industries of AI, space tech, and fintech.

Are you a private equity investor looking for actionable insights in today’s complex conditions? Let Eqvista assist you with a detailed portfolio valuation. In the six years since our inception, we have valued over 23,000 companies. Contact us today to learn more!