While NQDC audits declined in recent years, the updated guide and the IRS’s request for substantial budget increases suggest heightened enforcement may be forthcoming. If enacted, a proposal in the Biden administration’s budget would also require employers to withhold Section 409A penalties from employees’ pay starting in 2024.

IRS recently updated the Nonqualified Deferred Compensation Audit Techniques Guide in March 2024, AM 2024-001, providing new insights into its approach to audits of nonqualified deferred compensation (NQDC) plans, including those subject to Section 409A. Previously, the IRS updated its NQDC Audit Technique Guide, publication 5528, in June 2021, replacing the previous 2015 version. The 2021 guide provides a more detailed discussion of the legal authority surrounding nonqualified deferred compensation (NQDC) plans.

Expanded Discussion of Section 409A Requirements

The updated IRS guide provides an in-depth discussion of the principal requirements of Section 409A(a):

- Section 409A states that all deferred amounts under an NQDC plan for all taxable years must currently be included in gross income unless certain requirements are performed.

- Subsequent changes to the time or form of payment are allowed only if certain timing requirements are met.

- NQDC can only be paid upon the occurrence of a permissible payment event.

- Payment cannot be accelerated or delayed except as permitted by regulations.

- The rules of Section 409A apply to various service providers, including employees, independent contractors, and non-employee directors who earn deferred compensation.

Section 409A(b) Rules Regarding Certain Funding Arrangements

Newly updated IRS guide emphasizes few exceptions under Section 409A(b) where funding a nonqualified plan results in immediate taxation:

- The guide emphasizes three exceptions under Section 409A(b) where funding will result in immediate taxation and potential additional taxes

- Use of an offshore rabbi trust, unless substantially all services are performed in that foreign jurisdiction.

- Use of a “springing trust” where assets become restricted for NQDC payments upon a change in the employer’s financial health.

- Transfer of assets to a rabbi trust for executives at the expense of funding a single-employer defined benefit (DB) plan.

- Under IRC § 409A(b)(1), if the employer uses an offshore rabbi trust, NQDC is subject to taxation and additional taxes under IRC § 409A once the compensation becomes vested.

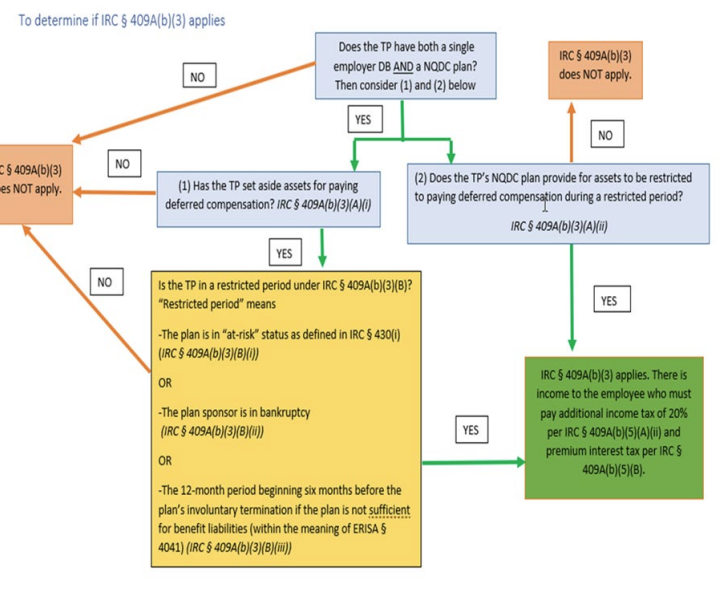

- Section 409A(b)(3) requires an examiner to review both the NQDC and any single-employer DB plan to know if an employer set aside assets to pay deferred compensation when in a restricted period .

Example for IRS Audit Technique Guide

The Nonqualified Deferred Compensation Audit Technique Guide provides an example and exhibits that auditors should review when examining nonqualified deferred compensation (NQDC) plans.

- Deferral Election Forms – Auditors should review the deferral election forms to determine if changes were requested and approved properly. This helps verify compliance with the timing rules under Section 409A.

- Executive Compensation Disclosures – Auditors should review the executive compensation disclosures in SEC filings, such as the company’s proxy statement. These can provide insights into the company’s NQDC arrangements.

- Executive Compensation Disclosures – Auditors should review the executive compensation disclosures in SEC filings, such as the company’s proxy statement. These can provide insights into the company’s NQDC arrangements.

- Forms W-2 – Auditors should examine Forms W-2 for proper timing of wage reporting related to NQDC distributions. Distributions are generally reported in Boxes 1, 2, and 11, while deferred amounts are reported in Boxes 3 and 5 for FICA taxes.

- Schedule M Adjustments

- Auditors should verify that the employer made appropriate Schedule M adjustments on its tax return: Deferrals are not deductible for the current year.

- For prior year distributions deducted in the current year

- This ensures the employer’s deduction timing matches the employee’s income inclusion.

The guide provides detailed instructions for auditors to examine these and other aspects of NQDC plans to assess compliance with Section 409A and proper tax treatment.

Simplify Non-Qualified Deferred Compensation Plan with Eqvista!

The updated audit guide arms the IRS with more robust tools to enforce strict compliance with the complex rules surrounding NQDC plans through heightened scrutiny of Section 409A, constructive receipt, funding mechanisms, reporting requirements, and more comprehensive audits if additional funding is obtained.

Accurate 409A valuations are critical for setting exercise prices of stock options issued under NQDC plans to comply with Section 409A rules and avoid penalties. By leveraging Eqvista’s specialized 409A valuation services, compliance guidance, equity management tools, audit support, and scalable solutions, companies can mitigate risks and costly penalties associated with operating NQDC plans that fail to meet the complex Section 409A requirements.