Venture capital has always been a risky asset class. The general consensus is that 90% of startups fail, and more than 66.67% of startups do not provide positive returns to investors. These risks pushed venture capitalists to develop a valuation method that secures desirable exits.

The importance of the venture capital (VC) valuation method has only increased in 2025. Since 2021, due to the reversal of global monetary policies, dealmaking activity has been subdued, making it challenging to secure exits. This is especially true for investors who entered the then-popular SaaS startups at high valuations during the zero-interest-rate period. These challenges are only accentuated due to the tariff-related tensions.

Hence, in this article, we will explore how the VC method can be utilized to enter new software startup investments at reasonable valuations, which leave room for fruitful exits.

Components of the VC method for software exit scenarios

The venture capital (VC) valuation method is used to value early-stage companies with limited financial histories. It incorporates investor expectations into the market-based valuation approach. As a result, it produces a valuation that is likely to secure the desired exit for the investor.

You can use this method to value software startups in the following manner:

Estimating the exit value

The first step in the VC valuation method is estimating the exit valuation. Ideally, you would want to base your valuations primarily on financial projections. However, since you are calculating a future valuation, this would mean building financial projections for a period well into the future. Since the accuracy of financial projections falls the farther you move from the historical data, you cannot base your exit valuation entirely on financial projections.

Instead, you must estimate the revenue or cash flow on the exit date and then apply an appropriate valuation multiple.

You must choose the exit date carefully by considering your own liquidity needs, market conditions, and venture capital industry norms. Typically, venture capitalists stay invested in a startup for up to 5 years.

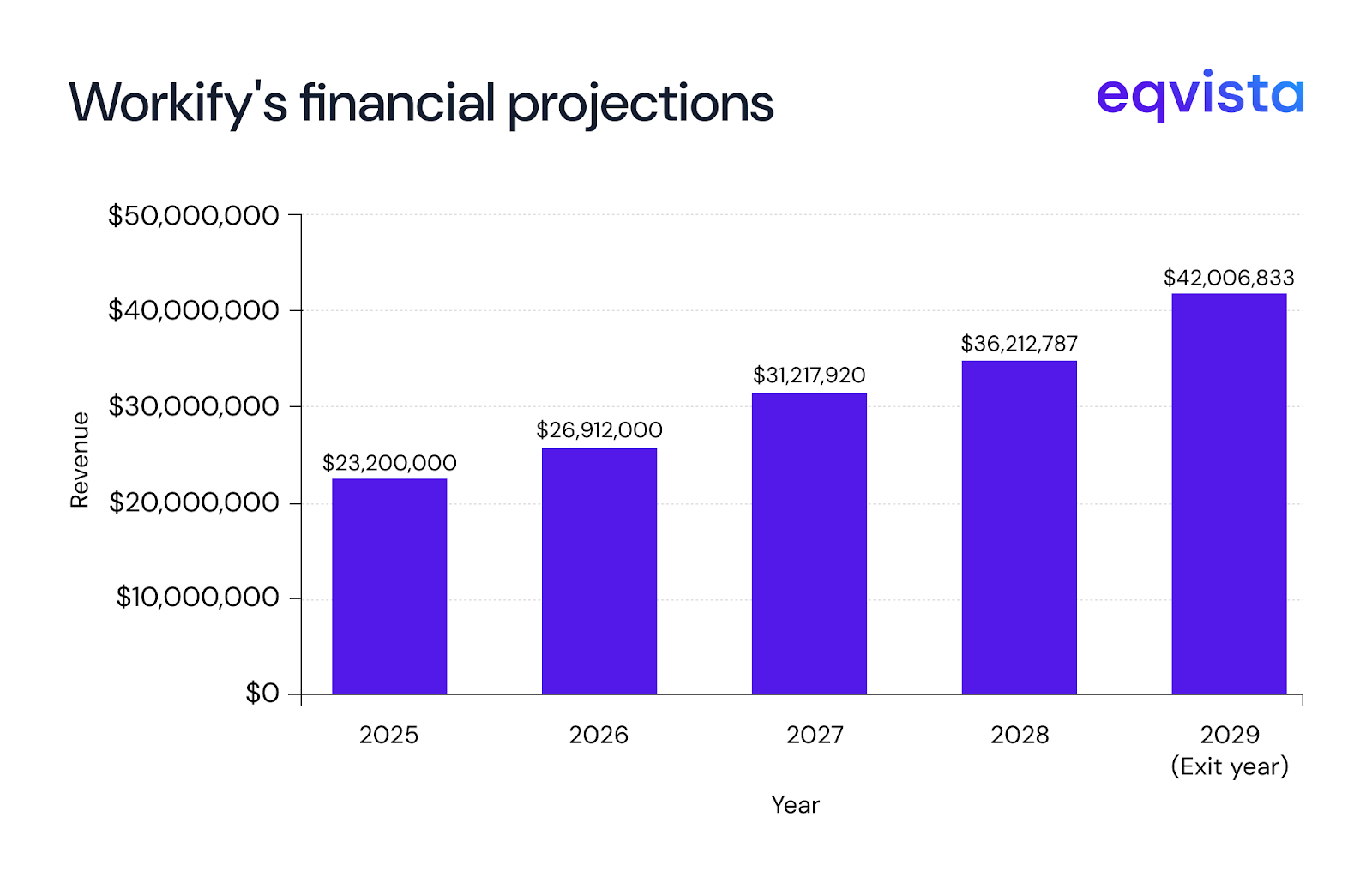

So, let us explore an example where the exit is expected in 5 years. Research suggests that the median EV/revenue ratio is 5.5 and the median revenue growth rate is 16%.

So, suppose you are looking to invest in Workify, a SaaS company that enables various programmers and non-programmers to collaborate seamlessly on tech projects. At present, Workify has an annualized revenue of $20 million.

Based on this information, we can make the following projections.

Now, we can calculate Workify’s enterprise value as = Exit year valuation × SaaS valuation multiple

= $42,006,833.15 × 5.5

= $231,037,582.34

Let us assume that Workify is debt-free and has negligible cash reserves. So, its exit valuation would be the same as its exit enterprise value.

Calculate target ROI

According to a Harvard study, more than 66.67% of startups do not generate positive returns for investors. To balance this risk, venture capitalists often seek high returns. While stock market investors would expect 12% to 15% returns, a venture capitalist would expect 25% to 35% returns.

You should determine the target return on investment (ROI) based on your portfolio needs, risk exposure, as well as returns prevalent in venture capital, private equity, and stock markets. Typically, private equity returns are higher than stock market returns to compensate for the higher risk. For the same reason, venture capital investments command a higher return than other private equity investments.

Discount to present value

Once you have identified the target ROI, you must use it to discount the exit valuation to the present value. Let us continue our example and assume a targeted ROI of 35%.

Then, Workify’s present valuation can be calculated as = Exit valuation/(1+Target ROI)Period of investment

= $231,037,582.34/(1+35%)5

= $231,037,582.34/4.48

= $51,524,500.33

Calculate post-money and pre-money valuations

You must note that the valuation of $51.52 million calculated in the previous step is the post-money valuation. In negotiations, it is extremely important to clearly define the post-money and pre-money valuations.

You can calculate the pre-money valuation from the post-money valuation by subtracting the investment amount. At this stage, you must check how much investment would fetch the desired level of ownership.

Let us continue our example and explore the pre-money valuations and ownership percentages when the investment amounts are $10 million, $15 million, and $20 million.

| Particulars | Case 1 | Case 2 | Case 3 |

|---|---|---|---|

| Post-money valuation | $51,524,500.33 | $51,524,500.33 | $51,524,500.33 |

| Investment amount | $10,000,000.00 | $15,000,000.00 | $20,000,000.00 |

| Pre-money valuation | $41,524,500.33 | $36,524,500.33 | $31,524,500.33 |

| Ownership percentage | 19.41% | 29.11% | 38.82% |

You should choose an ownership percentage depending on investment objectives.

Suppose this particular investment carries strategic importance, and you wish to influence the startup’s product development and deployment roadmap. Then, you should go for a high ownership percentage such as the one in Case 3.

If the only purpose of investing in Workify is to earn returns, a low ownership percentage, such as the one in Case 1, might suffice.

If you have substantial confidence in Workify and want to increase your total gains from this investment, you could choose a higher ownership percentage, such as the one in Case 2.

The choice of ownership percentage can be quite subjective.

Software Startup Exit Scenarios

Typically, a venture capitalist exits their software startup investments through one of the following three scenarios:

Mergers and Acquisitions (M&A)

The global M&A activity has been on a downward trend since 2021. This is primarily because of the reversal in global monetary policies. Back in 2021, central banks worldwide kept interest rates extremely low to spur economic activity during the COVID-19 pandemic. However, as the economy showed signs of recovery and inflation became a primary threat, central banks began hiking interest rates. As a result, it became challenging for companies to pursue M&A transactions through debt.

However, in 2024, M&A activity showed signs of recovery, increasing from $3.2 trillion in 2023 to $3.5 trillion in 2024.

Initial Public Offerings (IPO)

A very small percentage of startups make it to the IPO stage. To put things into perspective, only 8 VC-backed tech companies had IPOs in 2024, while 3,226 startups raised Series A funding. So, typically, venture capitalists do not count on IPOs for exits from software startup investments. However, IPOs are arguably the best exit scenario for venture capitalists.

Private Equity (PE) Investments or Buyouts

In the dearth of M&A activity and IPOs, private equity buyouts have emerged as a viable exit option for venture capitalists. In Q1 2025, the number of global private equity acquisitions increased by 45% while the value of such deals increased by 110.23% on a year-on-year basis.

Presently, a key roadblock to any kind of exit for venture capitalists is the uncertainty in startup valuations due to tariff tensions.

Best Practices for Software VC Exit Planning

Some of the best practices for planning software startup exits as a venture capitalist are as follows:

Plan Early

Unlike a few years ago, securing exits as a venture capitalist has become extremely challenging. As discussed earlier, this is primarily the result of interest rate tightening and tariff tensions. So, as a venture capitalist, you cannot afford to miss out on favorable exits. To do so, you must start planning for exits right from the deal sourcing phase.

Based on the prevailing market conditions, you must assess how long you would need to hold your investments. Then, you should identify the kinds of macroeconomic changes that would affect this timeline.

Focus on Financial Metrics

Due to the slowdown in dealmaking activity, most investors are likely to become risk-averse than before. Hence, they would prefer investing in commercially viable startups. So, when you invest in a software startup with strong financials, you would have better chances of securing exits.

Specifically, you should focus on software startups with reasonable customer acquisition costs and healthy revenue growth.

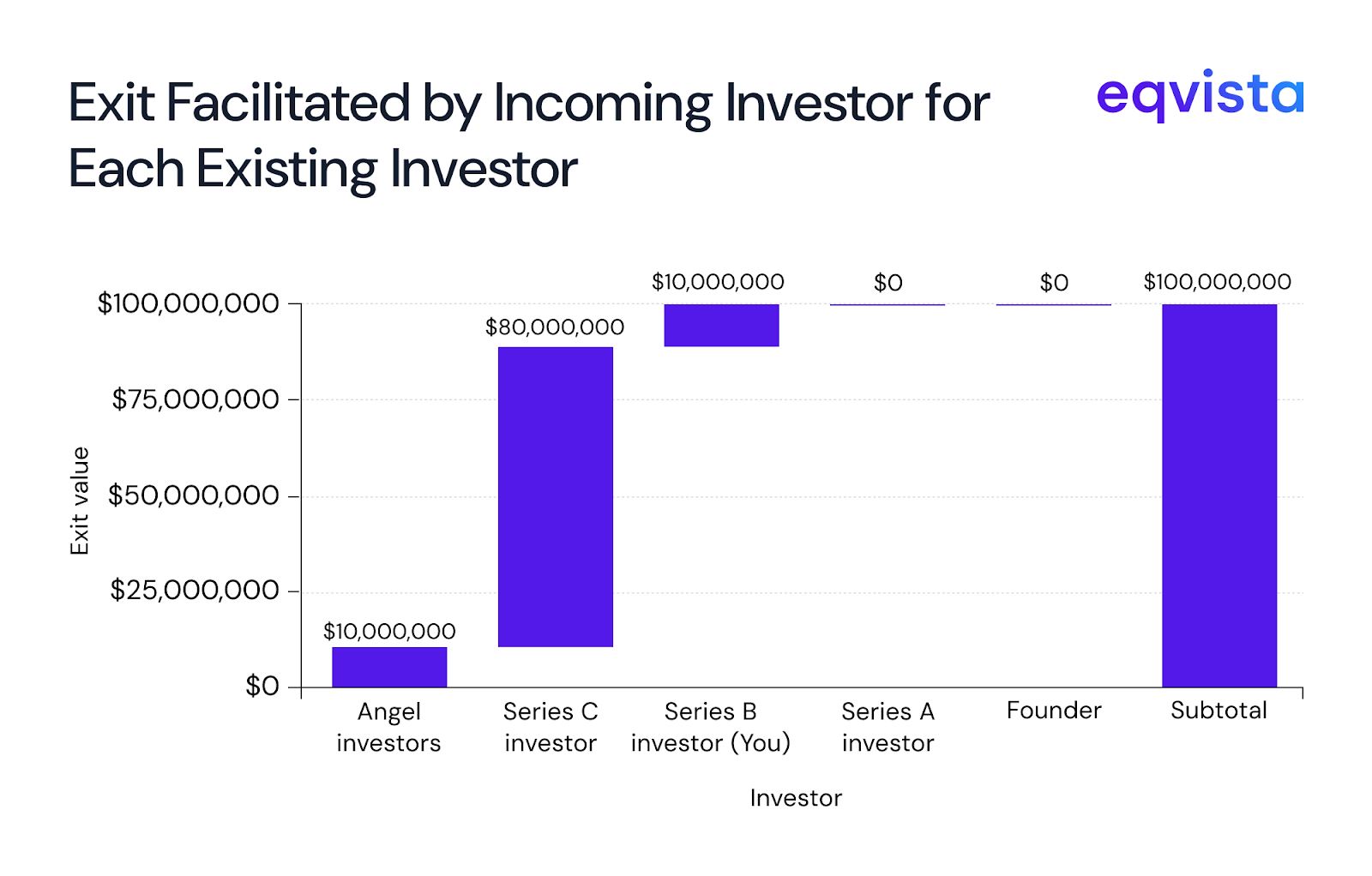

Use Waterfall Analysis

Exits from venture capital investments are seldom straightforward. Every new batch of investors would demand payout priority. Hence, you will need to investigate the payout hierarchy in your invested companies. Based on this hierarchy, you must perform waterfall analysis to estimate your exit value.

Suppose an incoming investor has agreed to facilitate exits worth $100 million at a share price of $10. Upon inquiry, you realized that your invested company has the following payout hierarchy:

| Priority | Investor | Shares held | Value of stake |

|---|---|---|---|

| 1 | Angel investors | 1,000,000 | $10,000,000 |

| 2 | Series C investor | 8,000,000 | $80,000,000 |

| 3 | Series B investor (You) | 4,000,000 | $40,000,000 |

| 4 | Series A investor | 2,000,000 | $20,000,000 |

| 5 | Founder | 6,000,000 | $60,000,000 |

By performing waterfall analysis, you would realize that the incoming investor would facilitate only a 25% exit ($10 million) for you. If you wish to increase your exit value, you may need to negotiate with the incoming investor or investors who are higher than you in the hierarchy.

Eqvista – Advantage through accuracy!

The accuracy of the VC method hinges on the quality of data. If you are valuing a seed-stage software startup, applying the stage-agnostic valuation multiples would result in overvaluations. At Eqvista, our seasoned valuation experts can help you avoid such disadvantageous scenarios. Our team has extensive experience in delivering accurate and data-backed valuations that are easily defendable at negotiation tables. Contact us to learn more about our services!