Intellectual property (IP) valuations aim to find out how well a company can monetize its research and development (R&D) results or reputation. IP rights, especially patents, are granted in such a way that companies are incentivized to keep innovating while other people have access to the technology and can improve on it eventually.

The incentives typically manifest in the form of a monopoly for the innovator or some kind of licensing power, and they are quite valuable. As it turns out, in 2023, intangible assets like intellectual property rights made up 90% of the enterprise value of the top 15 US companies.

You can understand the level of competitive advantage a company gets by valuing its IPs. Thus, IP valuations can be an important component of business valuations as well.

Through this article, we will go over the trends in IP, the factors that affect IP valuations, and the methods for valuing IPs. Then, we will show you how professionals perform IP valuations through a case study.

What is intellectual property?

Intellectual property (IP) is a category of intangible assets that you create using your mind. Some famous IPs are Coca-Cola’s secret formula for its cold drink, and Kentucky Fried Chicken’s (KFC) 11 secret herbs and spices. This form of IP is known as trade secrets.

If you follow tech firms and engineering firms, you may have heard about patents. IP also includes trademarks over symbols, names, and slogans that are linked to your product and form a basis for its reputation. Another form of IP rights is the copyright of authors and artists over their literary and artistic work.

When something is recognized as your IP, you get rights against duplication or imitation of said IP. Thus, IPs can be a source of competitive advantage. In some cases, companies will utilize their IPs to generate licensing income.

For example, pharma companies can attain patents over pharmaceutical ingredients and other products. Then, they can license other companies to produce and market said products for a licensing fee.

Some of the conditions for gaining IP rights are as follows:

| Type of intellectual property | Main Condition |

|---|---|

| Patents | The invention must not be known to the public or obvious to people in your industry, and it must have an industrial application |

| Trademarks | The trademark must be unique, distinctive, and non-deceptive, and must help identify the product it is registered for |

| Copyrights | Authors get copyright protection for their original work in tangible form, i.e. books can be copyrighted but not ideas |

| Trade secrets | The information must be commercially valuable, known only to a small group, and should be protected by the one who holds the IP right to it |

| Industrial designs | The design must be original |

Trends in IPs

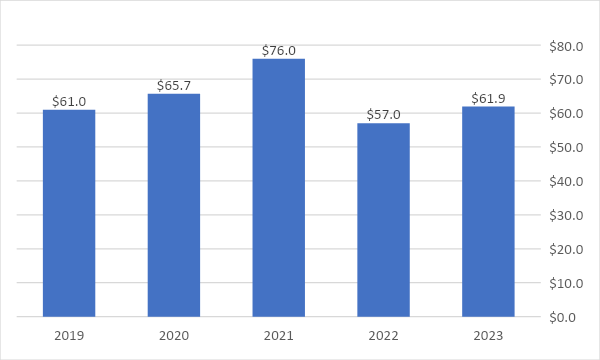

Intellectual property rights form a major part of the intangible assets of companies. According to Brand Finance, in 2023, the value of all intangible assets in the world was $61.9 trillion, rising 8.60% from the previous year. We can see the recent trends in intangible asset values in the chart below.

Source: Brand Finance

We can think of IP rights as being generated by the number of scientific and technical journal articles published. By this logic, Switzerland was the most efficient country in generating IP rights with more than 50 thousand such articles published per million people from 1996 to 2020. The United States and the United Kingdom do not even make the top 10 list.

Source: World Bank and United Nations via Our World in Data

However, if we talk about total scientific publications, the United States, China, United Kingdom, Japan, Germany, and France led the way from 2000 to 2020.

Scientific publications worldwide between 2000 and 2020

Source: World Intellectual Property Organization

What affects IP valuations?

IP valuation depends on how easily the IP can be enforced, the extent of competitive advantage they provide, and their licensing potential among other things. We will go over these factors in this section.

Market size and potential for growth

A large and expanding market offers substantial opportunities for revenue generation, which directly enhances the IP’s worth. In addition to the current size of the market, we must also consider its growth potential.

For example, in the healthcare or technology sectors, there can be high IP valuations because the demand is consistently increasing, and so are the anticipated future earnings.

Conversely, an IP in a stagnant or declining market may struggle to realize significant value despite its intrinsic merits.

Enforceability

Enforceability refers to how much protection you can get against unauthorized use or infringement of the IP right. An IP with robust protection in key jurisdictions will be highly valued as it offers security. Conversely, IPs with weak or uncertain enforceability are not as valuable.

Innovativeness and unique nature

An IP that introduces a novel solution, method, or brand distinct from existing offerings can command a premium in the market. This will not only attract customers but also create barriers to entry for competitors.

For example, a patent covering a groundbreaking technology that significantly advances an industry will be highly valued because it can create new markets or transform existing ones.

Stage of development

Early-stage IPs for which industrial application has not been explored or the market reaction has not been recorded have less value than late-stage IPs. This is because late-stage IPs will already be generating revenue and will have already demonstrated market viability. The company with late-stage IPs will know how much competitive advantage they can get from such IPs.

Licensing potential

IPs that can be easily licensed to multiple parties offer diversified revenue streams and reduce reliance on a single commercialization strategy. So, if a patent has various applications across industries, then the patent holder can issue licenses to various entities to generate revenue.

Competitive advantage

An IP right that enables the owner to outperform competitors holds substantial value. IPs can give you a competitive advantage by boosting your company’s offerings, improving brand value, differentiating the product from competitors, and improving cost efficiency.

Another example of high intellectual property valuation would be strong trademarks like Pepsi or Coca-Cola because the names of these brands have replaced the term ‘cold drink’ in most people’s vocabularies.

Similarly, if a patent enables a company to produce much cheaper than its competitors, the company can either benefit from higher margins or capture a greater market share by lowering its prices.

How are IP valuations determined?

IP valuation methodologies can be broadly categorized into three main approaches, which are the cost approach, market approach, income approach (typically the royalty relief approach). Each approach offers a unique perspective on IP valuation. At the same time, each method is suitable for different types of IPs. Let us learn more about them.

In this section, we will define each approach and see how they can be applied to valuing EcoGro Analytics. This is a product of EcoGro, a startup specializing in innovative software solutions for businesses to enhance productivity and efficiency. EcoGro Analytics is a proprietary software platform known for its advanced algorithms and user-friendly interface. The company seeks an intellectual property valuation for its software to attract investors and plan for future strategic moves.

Cost Approach

IPs like patents and industrial designs which are produced through research and development (R&D) investments can be valued using the cost approach. In this approach, we focus on the cost of reproducing or replacing the IP in question and we consider the time it will take for the IP to become obsolete. If obsolescence is far in the future, we will consider the validity period of the IP.

The cost approach to IP valuation is broadly divided into the replacement cost method and the reproduction cost method. In the reproduction cost method, we look at the investments made to create the IP right, whereas, in the replacement cost method we look at the cost to recreate the economic gains or utility gained from the IP.

The research and development expenses for the software over the years are shown below:

| Year | Research and Development Cost |

|---|---|

| 2004 | $24,342 |

| 2005 | $12,372 |

| 2006 | $13,256 |

| 2007 | $12,367 |

| 2008 | $15,684 |

| 2009 | $25,364 |

| 2010 | $15,478 |

| 2011 | $12,345 |

| 2012 | $12,365 |

| 2013 | $12,346 |

| 2014 | $22,678 |

| 2015 | $13,456 |

| 2016 | $12,678 |

| 2017 | $12,478 |

| 2018 | $22,789 |

| 2019 | $23,345 |

| 2020 | $11,567 |

| 2021 | $12,356 |

| 2022 | $12,567 |

| 2023 | $19,713 |

| 2024 | $18,334 |

The value of the intangible asset can be determined by considering the costs associated with creating and maintaining the software over the years.

| Year | Original Software and IT Cost |

|---|---|

| 2004-2022 | $299,833 |

| 2023 | $19,713 |

| 2024 | $18,334 |

| 2024 Valuation | $337,880 |

To understand things better, below is the unadjusted balance sheet of the company along with the adjustments made.

| Balance Sheet For the Year Ended Dec 31st ($) | 5/15/2024 | Adjustment | Adjusted 5/15/2024 |

|---|---|---|---|

| ASSETS | |||

| Current Assets | |||

| Cash and Cash Equivalents | 839,913 | - | 839,913 |

| Accounts Receivable | 631,309 | - | 631,309 |

| Total Current Assets | 1,471,222 | - | 1,471,222 |

| Non-Current Assets | |||

| Startup and Organizational Costs | 738,386 | - | 738,386 |

| Intangible Asset | - | 337,880 | 337,880 |

| Total Non-current Asset | 738,386 | 337,880 | 1,076,266 |

| TOTAL ASSETS | 2,209,609 | 337,880 | 2,547,489 |

| LIABILITIES & EQUITY | |||

| Current Liabilities | |||

| Accounts Payable | 355,457 | - | 355,457 |

| Short-term Loans | - | - | - |

| Accrued Expenses | 57,000 | 57,000 | |

| Total Current Liabilities | 412,457 | - | 412,457 |

| Long-term Liabilities | |||

| Long-term Debt | 180,000 | 180,000 | |

| Deferred Tax Liability | 90,000 | 90,000 | |

| Long-term liabilities | 270,000 | - | 270,000 |

| Total Liabilities | 682,457 | - | 682,457 |

| Stockholders' Equity | |||

| Opening Balance Equity | 387,000 | - | 387,000 |

| Retained Earnings | 120,190 | - | 120,190 |

| Shareholders' equity | 800,000 | - | 800,000 |

| Net Income | 219,962 | - | 219,962 |

| Revaluation of Intangible Asset | - | 337,880 | 337,880 |

| Total stockholders' equity | 1,527,152 | 337,880 | 1,865,032 |

| TOTAL LIABILITIES & EQUITY | 2,209,609 | 337,880 | 2,547,489 |

At this point, can get the shareholder’s equity value for the adjusted balance sheet.

| Before IP Valuation ($) | After IP Valuation ($) | |

|---|---|---|

| Total Assets | 2,209,609 | 2,547,489 |

| Total Liabilities | 682,457 | 682,457 |

| Revaluation of Intangible Asset | - | 337,880 |

| Total Stockholders' Equity (Total Assets – Total Liabilities) | 1,527,152 | 1,865,032 |

Thus, from a balance sheet perspective, the software is worth $337,880 after adjustments.

Market approach

Any type of IP that is actively bought and sold like brand names, patents, and industrial designs can be valued using the market method. This is probably the simplest approach available. It can be quite useful in negotiating IP deals.

However, IPs are meant to be unique and hence you may struggle to find comparable transactions which limits the applicability of this approach.

If you cannot find similar IPs sold under similar market and economic conditions, you may have to make several assumptions and adjustments that will reduce the reliability of such an IP valuation.

To value EcoGro Analytics, we will first research similar software that were sold in the market. By doing so, we will end up with the following table:

| Software Name | Software Description | Acquirer | Transaction Value (in Millions) | Year | Estimated Royalty Rate (%) |

|---|---|---|---|---|---|

| Tableau | Interactive data visualization software company focused on business intelligence. | Salesforce | $15,700 | 2019 | 10-12% |

| Looker | An enterprise platform for business intelligence, data applications, and embedded analytics. | $2,600 | 2019 | 8-10% | |

| Qlik | Business Intelligence and data integration platform. | Thoma Bravo | $3,000 | 2016 | 8-10% |

| Adaptive Insights | Automates consolidations and integration of data. | Workday | $1,550 | 2018 | 7-9% |

| TIBCO | Provides enterprise application integration, data virtualization, and business process automation capabilities. | Vista Equity Partners | $4,300 | 2014 | 8-10% |

| Alteryx | Data analytics and visualization platform offers a wide range of tools to help businesses. | Clearlake Capital Group Insight Partners | $4,400 | 2024 | 9-11% |

| Median | 8.00% | ||||

| Average | 8.33% |

This table gives a snapshot of significant transactions involving analytics software companies, providing insights into their market valuation through acquisition. However, specific royalty rates, which are often confidential and subject to negotiation, are not typically disclosed publicly.

Based on the comparable analysis for EcoGro Analytics software, it has a good standing compared to other software.

Income approach

The income approach involves estimating the future income from an asset, discounting it, and then subtracting the cost of generating the IP. Factors such as market demand, competitive advantage, and the lifespan of the IP are considered in this approach to IP valuation.

The IP valuation methods under the income approach are broadly classified under direct capitalization methods and discounted cash flow (DCF) methods.

Such an approach applies to an IP asset that already has positive net cash flows. A key limitation of this approach is that it is difficult to choose a discount rate that truly reflects the risk of the IP becoming obsolete.

Royalty Relief Method

The royalty relief approach to IP valuation determines hypothetical royalty payments that would be avoided if the asset were owned rather than licensed. It is based on owning an intangible asset eliminating the need for the company to pay for licensing it.

Let us assume that the company has to pay a royalty rate of 8.33% if it licenses the software.

| Royalty Rate | 8.33% |

| Useful Life of Software | 5 Years |

| Weighted Average Cost of Capital (WACC) | 21.15% |

| Savings for the Company | $1.15M |

| Adjusted Forecast Figure ($) | 2024 | 2025 | 2026 | 2027 | 2028 | |

|---|---|---|---|---|---|---|

| Total D2P Subscription | $597,032 | $2,450,983 | $5,567,197 | $9,816,654 | $15,477,948 | |

| Royalty Rate | 8.33% | $49,733 | $204,167 | $463,748 | $817,727 | $1,289,313 |

| Tax | 21% | -$10,444 | -$42,875 | -$97,387 | -$171,723 | -$270,756 |

| Post-Tax Royalty Saving | $39,289 | $161,292 | $366,361 | $646,005 | $1,018,557 | |

| WACC | 21.15% | 0.8254 | 0.6813 | 0.5624 | 0.4642 | 0.3832 |

| Present Value | $32,430 | $109,892 | $206,034 | $299,876 | $390,273 | |

| Sum of Present Value | $1,038,505 | |||||

| Amortization | $197,639 | $197,639 | $197,639 | $197,639 | $197,639 | |

| Tax Rate | 21% | 21% | 21% | 21% | 21% | |

| TAB | $41,504 | $41,504 | $41,504 | $41,504 | $41,504 | |

| Present Value of TAB | $34,259 | $28,278 | $23,341 | $19,266 | $15,903 | |

| Sum of Present Value of TAB | $121,047 | |||||

| Present Value of Software | $1,159,551 |

From the royalty relief method, the Company would save $1,159,551 by owning the software instead of licensing it.

Unlock the True Value of Innovation with Eqvista’s Expert IP Valuation Services

Intellectual property valuation is a critical process for understanding your potential to monetize your innovations and competitive advantages.

Through various methods such as the cost, market, income, and royalty relief approaches, professionals perform IP valuations effectively.

Each method offers unique insights and is suitable for different types of IP. Through accurate IP valuations, companies can make informed strategic decisions, attract investors, and negotiate better deals.

The case study of EcoGro Analytics demonstrates the practical application of IP valuation methodologies and highlights the importance of IP in enhancing a company’s market position and financial performance.

If you need an IP valuation to facilitate a software transaction or to raise funds, contact Eqvista, the IP valuation expert.