Recently, OpenAI became the world’s second-most valuable startup after a $40 billion funding round, reaching a valuation of $300 billion. In 2025, we are no strangers to such headlines regarding AI startups. For instance, Safe Superintelligence reached a valuation of $32 billion without even having a product.

With such strong hype surrounding the sector, keeping oneself grounded can be extremely crucial. This article will discuss how to value AI startups in 2025 accurately.

Why is the income-based approach appropriate for valuing AI startups?

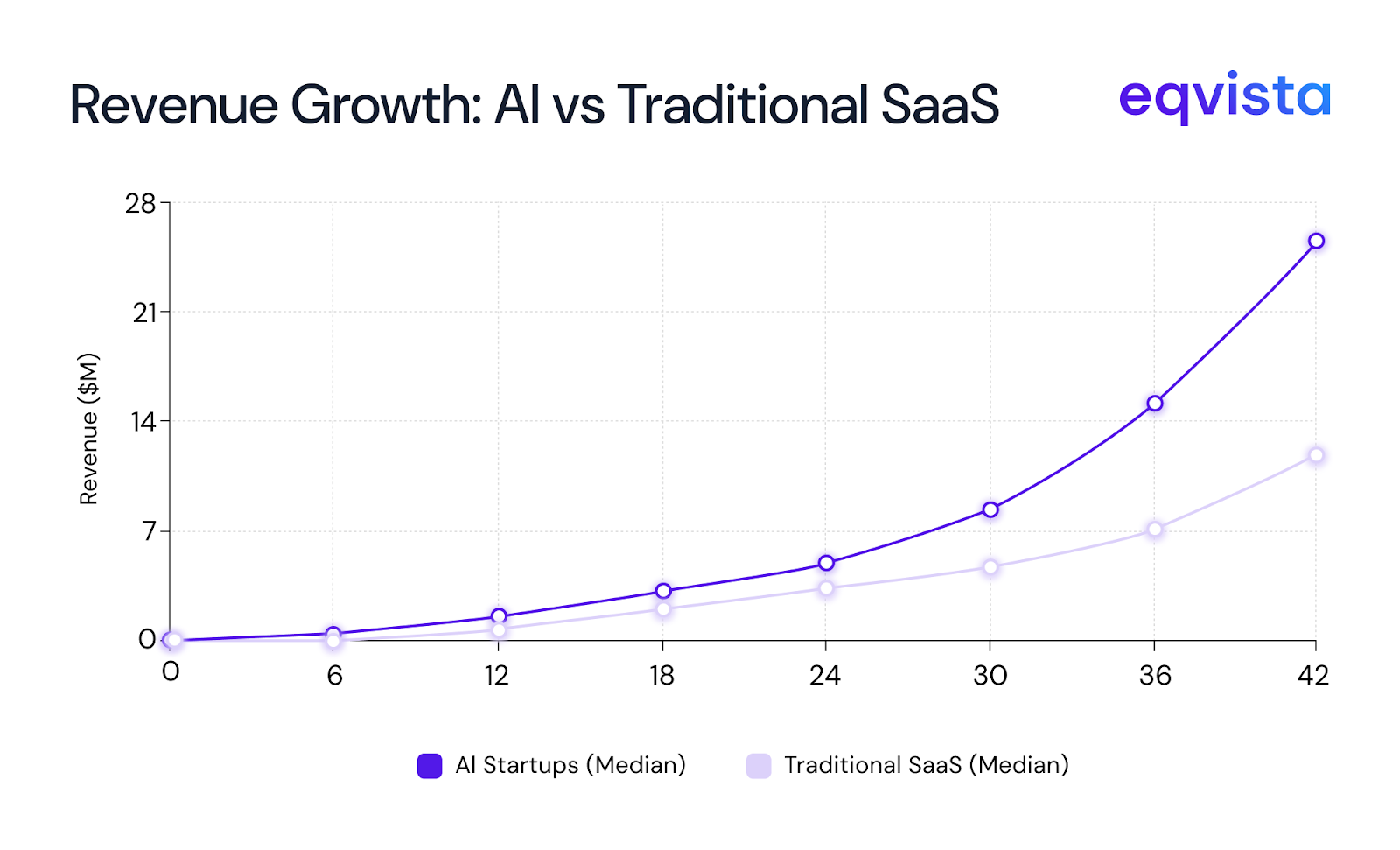

Due to the high commercial viability of AI startups, they are able to reach key revenue milestones at an unprecedented pace. For instance, in just three years, Cursor reached annual recurring revenue (ARR) of $100 million. Examples of even faster commercialization do exist. Bolt, the AI app and website-building platform, reached an ARR of $20 million in just 2 months.

These trends hold up even when we take a more generalized view. Stripe’s data suggests that the median time to reach $5 million in annualized revenue for the top 100 AI startups (by revenue) was 24 months. In contrast, the top 100 SaaS startups (by revenue) of 2018 had a median time of 37 months for reaching $5 million in annualized revenue.

This depth of revenue history makes it easy to produce accurate results with the income-based approach.

The income-based approach involves building cash flow projections based on financial history, macroeconomic factors such as interest rates and GDP growth rate, and industry trends. Then, the projected cash flows are discounted to the present value and summed to arrive at the company’s valuation. Typically, the required rate of return is taken as the discount rate.

Example: Income-based Approach for valuing AI Startups

Let us understand this methodology using an example. Suppose that the financial performance of the AI startup you wish to value can be summarized as follows:

| Period | 2024 |

|---|---|

| EBITDA | $1,000,000 |

| Depreciation and amortization (D&A) | $100,000 |

| Earnings before interest and taxes (EBIT) | $900,000 |

| Tax rate | 21% |

| Tax | $189,000 |

| Earnings before interest (EBIT-T) | $711,000 |

| Depreciation and amortization (D&A) | $100,000 |

| Net working capital | $200,000 |

| Capital expenditures | $400,000 |

| Unlevered free cash flows (UFCF) | $211,000 |

The UN expects the global AI market to grow at a compounded annual growth rate (CAGR) of 38.19% until 2033. We will assume that the AI startup being valued would outperform the market and achieve an EBITDA growth rate of 57.29%, 1.5 times the global AI market growth rate. We will also assume constant capital expenditure and net working capital, while the depreciation and amortization (D&A) increases 10% every year.

We will also assume that the startup can be expected to be in operation for 5 years.

Based on this, we can make the following cash flow projections.

| Period | 2025 | 2026 | 2027 | 2028 | 2029 |

|---|---|---|---|---|---|

| Earnings before interest, taxes, depreciation, and amortization (EBITDA) | $1,572,900 | $2,474,014 | $3,891,377 | $6,120,747 | $9,627,323 |

| Depreciation and amortization (D&A) | $110,000 | $121,000 | $133,100 | $146,410 | $161,051 |

| Earnings before interest and taxes (EBIT) | $1,462,900 | $2,353,014 | $3,758,277 | $5,974,337 | $9,466,272 |

| Tax rate | 21% | 21% | 21% | 21% | 21% |

| Tax | $307,209 | $494,133 | $789,238 | $1,254,611 | $1,987,917 |

| Earnings before interest (EBIT-T) | $1,155,691 | $1,858,881 | $2,969,039 | $4,719,726 | $7,478,355 |

| Depreciation and amortization (D&A) | $110,000 | $121,000 | $133,100 | $146,410 | $161,051 |

| Net working capital | $200,000 | $200,000 | $200,000 | $200,000 | $200,000 |

| Capital expenditures | $400,000 | $400,000 | $400,000 | $400,000 | $400,000 |

| Unlevered free cash flows (UFCF) | $665,691 | $1,379,881 | $2,502,139 | $4,266,136 | $7,039,406 |

At the end of the forecast period, the startup is expected to have the following assets and liabilities.

| Particulars | Value |

|---|---|

| A. Assets | |

| Proprietary AI models | $6,000,000 |

| Brand and domain name | $1,000,000 |

| Software IP | $3,000,000 |

| Office equipment | $250,000 |

| Cash reserves | $2,500,000 |

| Accounts receivable | $2,000,000 |

| Total assets | $14,750,000 |

| B. Liabilities | |

| Loans | $2,000,000 |

| Accounts payable | $300,000 |

| Accrued salaries | $200,000 |

| Total liabilities | $2,500,000 |

Based on this, we will calculate the terminal value as the asset-based valuation at the end of the forecast period.

Terminal value = Asset-based valuation at the end of the forecast period

= Total assets – Total liabilities

= $14,750,000 – $2,500,000

= $12,250,000

We will assume that investors have low growth expectations and set a discount rate of 10%. Then, we can estimate the valuation as follows:

| Year | Unlevered free cash flows (UFCF) | Discounting factor | Discounted cash flow |

|---|---|---|---|

| 2025 | $665,691 | 1.1 | $605,174 |

| 2026 | $1,379,881 | 1.21 | $1,140,398 |

| 2027 | $2,502,139 | 1.331 | $1,879,894 |

| 2028 | $4,266,136 | 1.4641 | $2,913,829 |

| 2029 | $7,039,406 | 1.61051 | $4,370,917 |

| 2029 (Terminal value) | $12,250,000 | 1.61051 | $7,606,286 |

| Valuation | $18,516,498 |

So, even when an AI startup significantly outpaces the overall market growth and investors have low return expectations, the EBITDA valuation multiple reaches only 18.52x. This goes to show how unrealistic some of the growth expectations would be for certain AI startups.

Challenges in applying a market-based approach to AI startup valuation

Valuing an AI startup using the market-based approach can be challenging due to the extremely high valuation multiples commanded by certain AI startups. For instance, Hugging Face has a valuation multiple of 150x. In the past, startups such as Anysphere, Physical Intelligence, and Perplexity had valuations greater than 500x their respective revenues. Such high valuation multiples are probably the result of investors coming to expect rapid commercialization and revenue growth with AI startups.

Hence, overvaluation is a key concern when using the market-based approach for AI startup valuation.

One way to avoid this would be to account for how the startup in question stands out from the market. This would involve accounting for differences regarding patent portfolio, growth potential, or other key factors. For instance, OpenAI has a valuation multiple of 30x, much lower than that of Hugging Face. The key difference between these companies would be the fact that OpenAI is a relatively mature startup and is already a market leader. Hence, Hugging Face would have a relatively higher expected growth rate.

Example: Market valuation multiple for AI startup valuation

Let us understand how you can use the market valuation multiple for AI startup valuation with an example.

First, you must shortlist the AI startups with the same funding stage and industry segment. Then, you must divide the total valuations of these startups by their total revenue to arrive at the market valuation multiple.

Suppose you are valuing InnovaFlow, an AI and cloud-based operational planning platform. This startup’s last funding round was a Series B round, and its annualized revenue is $10 million. Your research suggests that the peers of this startup had the following annualized revenues and valuations.

| Company name | Annualized revenue (in millions) | Valuations (in millions) |

|---|---|---|

| CloudOpsIQ | $15 | $1,020 |

| StratifyAI | $17 | $323 |

| NimbusLogic | $11 | $143 |

| PlanForge | $16 | $192 |

| SynapseOps | $13 | $143 |

| AetherPlan | $19 | $323 |

| OptiFlow | $19 | $380 |

| CloudMinds | $11 | $165 |

| IntelliOps | $20 | $320 |

| NovaGrid | $15 | $270 |

| Total | $156 | $3,279 |

Based on this data, we can calculate the market valuation multiple as = Total valuation of all startups in the market/Total revenue of all startups in the market

= $3,279 million/$156 million

≈ 21.02

Now, we can calculate InnovaFlow’s valuation as = InnovaFlow’s annualized revenue × Market valuation multiple

= $10 million × 21.02

= $210.2 million

How to value pre-revenue AI startups?

The ideal valuation methodology for pre-revenue AI startups could be the scorecard method. While this method might be subjective, its ability to combine market data with qualitative factors can prove valuable. You must take the following steps to value an AI startup using the scorecard method:

- Make a dataset of similar startups and their valuations

- Select the startup with the median pre-money valuation

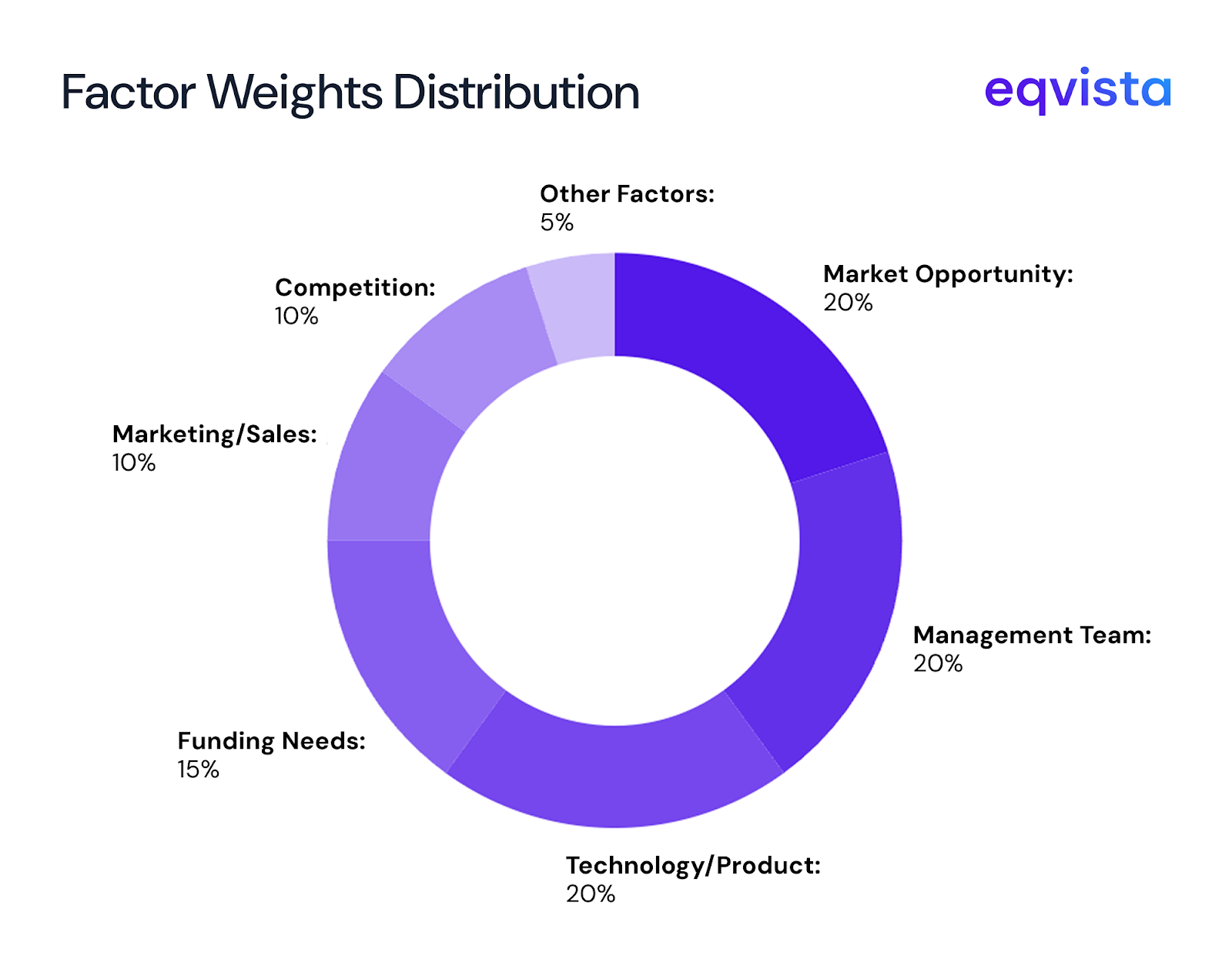

- Evaluate how your startup compares to the selected startup with respect to the following factors:

- Board, entrepreneur, and the management team

- Size of the opportunity

- Technology/Product

- Competitive environment

- Marketing/Sales

- Need for additional financing

- Others

- Based on your assessment, assign a percentage score for each factor. For instance, if your startup outperforms the selected startup in terms of ‘technology/product’, you can assign a score of 150%.

- Assign weights for each factor.

- Take the weighted sum of all scores.

- Multiply the median pre-money valuation by the weighted sum to arrive at your startup’s valuation.

Let us understand this method with an example. Suppose the median pre-money valuation for startups similar to Clover AI is $10 million. By comparing the Clover AI with the startup that had the median pre-money valuation, you come up with the following scores and weights.

| Factor | Score | Weight | Weighted score |

|---|---|---|---|

| Board, entrepreneur, and the management team | 110% | 20.00% | 22% |

| Size of the opportunity | 140% | 20.00% | 28% |

| Technology/Product | 100% | 20.00% | 20% |

| Competitive environment | 125% | 10.00% | 13% |

| Marketing/Sales | 100% | 10.00% | 10% |

| Need for additional financing | 150% | 15.00% | 23% |

| Others | 130% | 5.00% | 7% |

| Total weighted score | 122% |

Then, Clover AI’s valuation can be calculated as = Median pre-money valuation × Total weighted score

= $10 million × 122%

= $12.2 million

Eqvista- Unlocking value with accuracy!

The best way to determine an AI startup’s valuation is the same way great AI models are built: based on cold, hard data. By taking a data-centric approach, you can separate hype from value and make informed investing decisions.

This is an area where Eqvista excels. Every month, we deliver data-backed and actionable valuation reports for client assets worth over $2 billion. Contact us to know more!