Private equity investments, especially in startups, are notoriously illiquid. If a startup grows big enough, investors may breathe easy hoping for exits through initial public offerings (IPOs). However, trends are showing a significant decline in IPO volume and proceeds. Many startups are delaying their IPOs. This IPO dry spell has left investors searching for alternative forms of liquidity.

In response, Stripe explored a very unconventional method in the form of secondary share sales to provide exits for their investors.

In this article, we will explore how private equity players are pursuing such unconventional and creative ways to provide liquidity to investors, given the current state of the IPO market. Read on to know more!

Dried-up IPO market

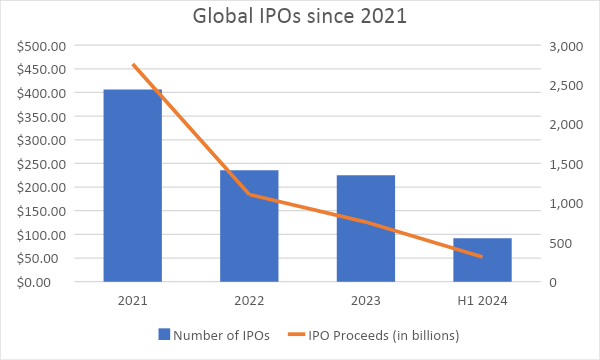

Since 2021, globally, IPO volume and proceeds have both been on the decline. Let us assume that H2 2024 will be a repeat of H1 2024. Then, in 2024, IPO volume will be half of that in 2021. Moreover, IPO proceeds will be less than a quarter of that in 2021.

Source: EY

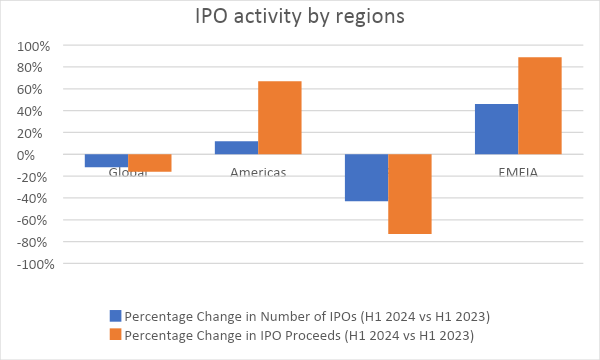

In H1 2024, the YoY drop in IPO proceeds and volume is coming out of the Asia-Pacific region. While the Americas and EMEIA (Europe, the Middle East, India, and Africa) have shown recovery, Asia-Pacific has seen drastic drops in IPO volume and proceeds.

Source: EY

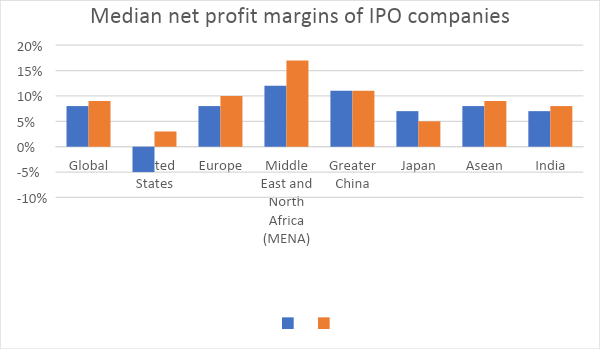

However, the situation might be taking a turn for the better. Globally, the median net profit margins of IPO companies have improved in H1 2024 over 2023. The median net profit margins declined only in Japan, a country going through a significant shift in monetary policy. For the first time in 17 years, the Japanese central bank raised interest rates.

Source: EY

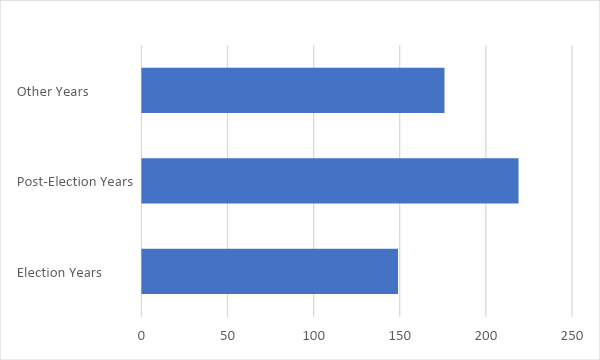

Typically, IPOs are lower in election years. Data suggests that post-election, there is a significant surge in IPOs. 2024 has been called the year of elections by many as nearly 1.5 billion people will cast their votes this year. So, we can expect IPOs to resume in 2025.

Source: EY

Sequoia offers payday to Stripe investors

Although we expect IPOs to rise in 2025, the post-election year, there are no guarantees. In such a situation, unicorns have had to become creative to provide exits to their investors and their employees.

A recent example of this would be Sequoia’s offer to buy shares owned by Stripe’s investors. Recently, Sequoia offered to buy $861 million worth of shares from its limited partners in funds raised between 2009-11. While extending this offer, Sequoia noted that Stripe’s latest 409A valuation was $70 billion and its stake in Stripe was valued at $9.8 billion.

Stripe is a 15-year-old startup that raised $6.5 billion in a Series I funding in 2023 at a valuation of $50 billion. ‘15-year-old’ and ‘Series I’ are not terms we often use to describe a startup. It is almost impressive how long Stripe has managed to stay private despite its size and success.

In February this year, Stripe issued a tender offer to buy shares worth more than $1 billion from its current and former employees. This repurchase was also meant to make up for the dilution caused by the Series I funding round.

For quite some time, the markets have anticipated Stripe’s IPO. In January 2023, the startup itself set a 1-year deadline to go public. Stripe intended to pursue private market transactions like fundraising rounds or tender offers if it could not go public.

Seeing how Stripe issued a tender to repurchase shares and Sequoia offered to buy shares owned by Stripe’s investors, Stripe’s IPO seems to be a long way off.

In a situation where even Stripe, one of the highest-valued startups in the world, is pushing off its IPO, investors in other, lesser-valued, and lesser-known startups would be facing extreme difficulty in making their exits.

Other creative exits being pursued

Some of the other creative ways in which startups and venture capital firms are offering exits to investors are as follows:

Direct listing

In a direct listing, a company’s existing shares are listed on public exchanges, and no new shares are offered. Here, the goal of most companies is to provide liquidity to their shareholders and not to raise funds. In recent times, Instacart had considered a direct listing before going for an IPO.

In September last year, the delivery and pick-up company achieved a valuation of nearly $10 billion when it raised $660 million. Currently, under the ticker of ‘NASDAQ: CART’, the company is trading almost 16% above its listing price.

Direct listings are not entirely uncommon for startups. High-profile startups like Spotify, Slack, Roblox, Coinbase, SquareSpace, and Amplitude have also gone for direct listings in the past.

Direct listing is a good hands-off approach for providing liquidity to investors. It does not require startups to set up transactions that would require them to use up their funds or find incoming investors.

Secondary market share sale

Back in June, SpaceX issued a tender offer to sell the shares of its investors at a share price of $112 and a valuation of $210 billion. Forbes reported that the size of this secondary market share sale had not been fixed and would be based on the interest shown by existing shareholders and outside buyers.

We can divide secondary market share sales into two types, the ones facilitated by the startup itself, and the ones pursued by the investors independently. Ideally, the party with a better network of accredited investors and private equity (PE) firms should facilitate the transactions.

While providing liquidity to investors, secondary market share sales do not significantly alter the startup’s ownership structure nor do they increase disclosure requirements like listings would. Hence, startups who want to put off their IPO to a later date will find secondary market share sales as a viable alternative.

Buybacks

As mentioned earlier, Stripe conducted a buyback intending to buy shares worth more than $1 billion from its current and former employees in February this year. In December 2023, ByteDance, TikTok’s parent company, announced a buyback of shares worth $5 billion at a valuation of $268 billion.

The company announced a buyback program for its US employees in March this year and later in April, it extended the program to employees outside the US.

There are two advantages to buybacks. Firstly, it helps the startup maintain control over its operations by reducing dilution. Secondly, if buybacks are announced regularly, employee stock options appear more liquid and thus, more attractive to employees. This can go a long way in attracting and retaining talent.

Eqvista: Unlocking Exit Opportunities with Reliable VC Valuations

Since 2021, IPOs have been on the decline, and in 2024, we expect the IPO proceeds to fall short of a quarter of IPO proceeds in 2021. In H1 2024, although Americas and EMEIA have shown considerable improvements in IPO volume and proceeds over the same period last year, Asia-Pacific faced the steepest drops in both metrics.

We can expect this IPO dry spell to give way in 2025, the post-election year, however, investors have grown anxious for exits and may not want to wait another year.

In response to this dry spell, Sequoia offered a payday to its limited partners invested in Stripe, the payments giant. Other startups like SpaceX and ByteDance are offering creative exits in the form of buybacks, direct listings, and secondary market share sales.

If you are someone trying to set up a secondary market share sale, you must know the difficulties in establishing a valuation. As a reputed third-party valuation expert, Eqvista can provide credible valuation reports that can go a long way in securing an exit. Contact us to know more!