With the provisions of the Tax Cuts and Jobs Act expiring by the end of 2025, the gift and estate tax exemption limit could drop from $13.99 million to just $7 million. High net worth individuals need to accelerate their estate planning efforts by leveraging trusts to minimize tax liabilities. People often underestimate the impact of trust valuations on the tax burden of the beneficiaries.

This article will discuss how trust valuations influence tax outcomes and why the tax benefits of commonly used trusts often depend on accurate and defensible valuations. Read on to know more!

How do trust valuations impact tax liabilities?

Typically, trust valuations impact tax liabilities of beneficiaries in two ways, which are:

Locking in asset values

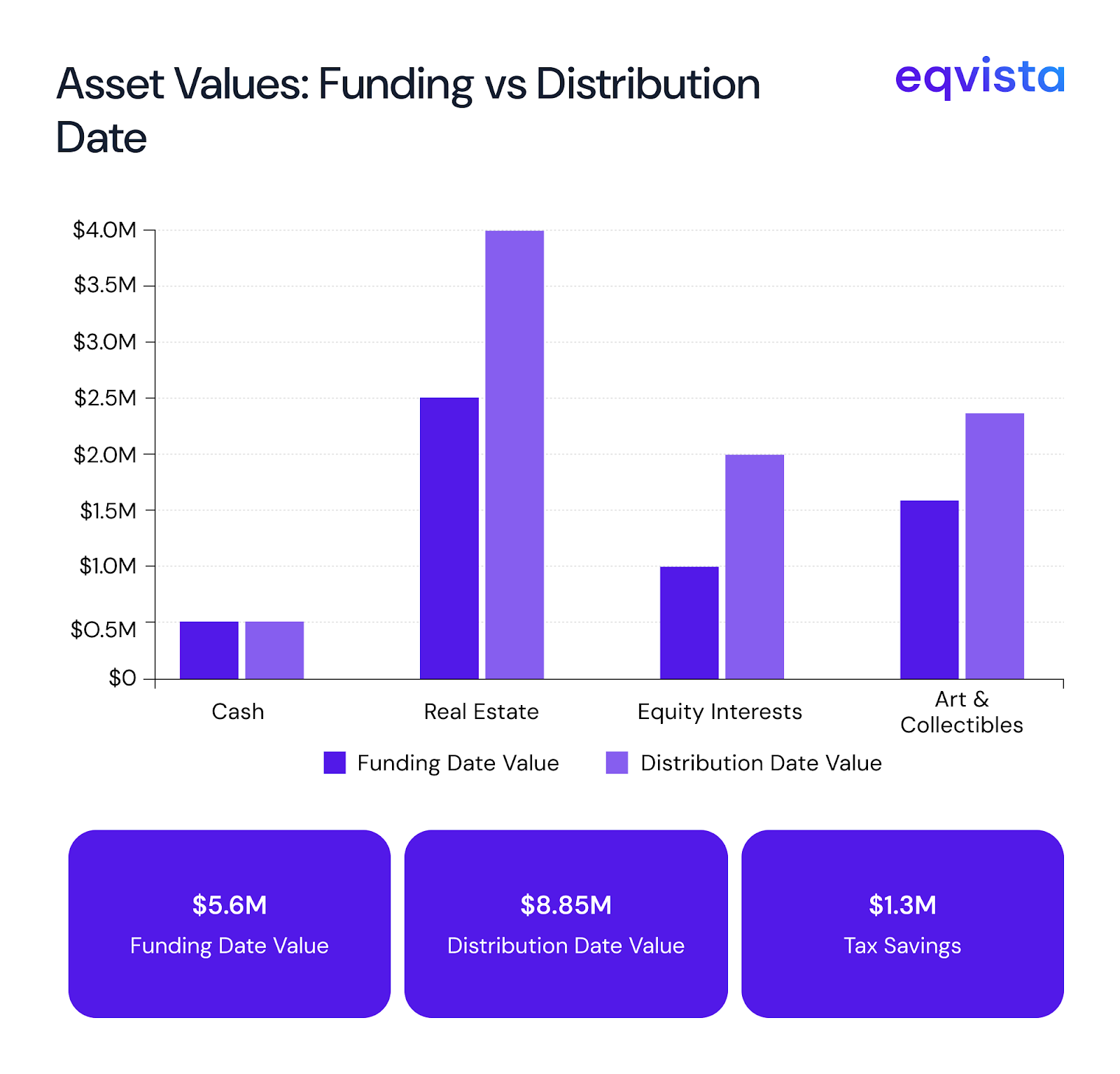

When assets are transferred to certain trusts, the estate tax is calculated as per the asset’s valuation on the funding date and not on the distribution date. As a result, any gains in value between the funding date and distribution would not be taxed.

Suppose, on funding date, the values of assets in a trust were as follows:

- Cash = $500,000

- Residential properties = $2.5 million

- Equity interests = $1 million

- Art and other collectibles = $1.6 million

Five years later, on the distribution date, these same assets are expected to have the following values:

- Cash = $500,000

- Residential properties = $4 million

- Equity interests = $2 million

- Art and other collectibles = $2.35 million

Let us explore the difference in tax liability depending on the taxation date.

| Particulars | Funding date | Distribution date |

|---|---|---|

| Cash | $500,000 | $500,000 |

| Real estate | $2,500,000 | $4,000,000 |

| Equity interests | $1,000,000 | $2,000,000 |

| Art and other collectibles | $1,600,000 | $2,350,000 |

| Trust valuation (Total asset value) | $5,600,000 | $8,850,000 |

| Tax liability on the first million dollars | $345,800 | |

| Tax rate for amounts over $1 million | 40% | |

| The amount on which the 40% estate tax rate is applicable (Trust valuation - $1 million) | $4,600,000 | $7,850,000 |

| Tax on the amount exceeding $1 million | $1,840,000 | $3,140,000 |

| Total tax liability | $2,185,800 | $3,485,800 |

You might notice that minimizing the funding date trust valuation can further reduce the estate tax liability.

Maximizing the benefits of the lifetime gift and estate tax exemption limit

In 2025, the exemption for gift and estate tax limit stands at $13.99 million. Any gifts and estate transfers under this limit are not taxed. However, any gift or estate transfer beyond this limit can attract a tax of 18% to 40%. So, to minimize your tax liability in estate planning, you must, once again, minimize your trust valuation.

Types of trusts and their tax benefits

In this section, we will discuss some of the commonly used types of trusts for estate planning. The valuations of each of these trusts are a key factor in determining tax liabilities.

Grantor Retained Annuity Trusts (GRATs)

Grantor Retained Annuity Trusts (GRATs) pay an annuity- paid through interest earned on the assets in the trust or through a portion of the assets – to the grantor for the term of the trust, after which its assets are distributed to the beneficiaries.

The transfer of any assets placed in a GRAT is taxed at the fair market value on the gift date. As a result, any growth in the value of assets post the gift date does not attract any taxes.

However, you must note that assets in a GRAT become a part of the grantor’s estate upon their death, and thus, their transfer does not carry the same tax benefit. So, a GRAT should be established only if the grantor is expected to survive the trust’s length.

Transfers of assets through GRATs are subject to the exemption of lifetime gift and estate tax as well as the annual gift tax exclusion. So, you can negate the tax liabilities from a GRAT by minimizing the GRAT’s valuation.

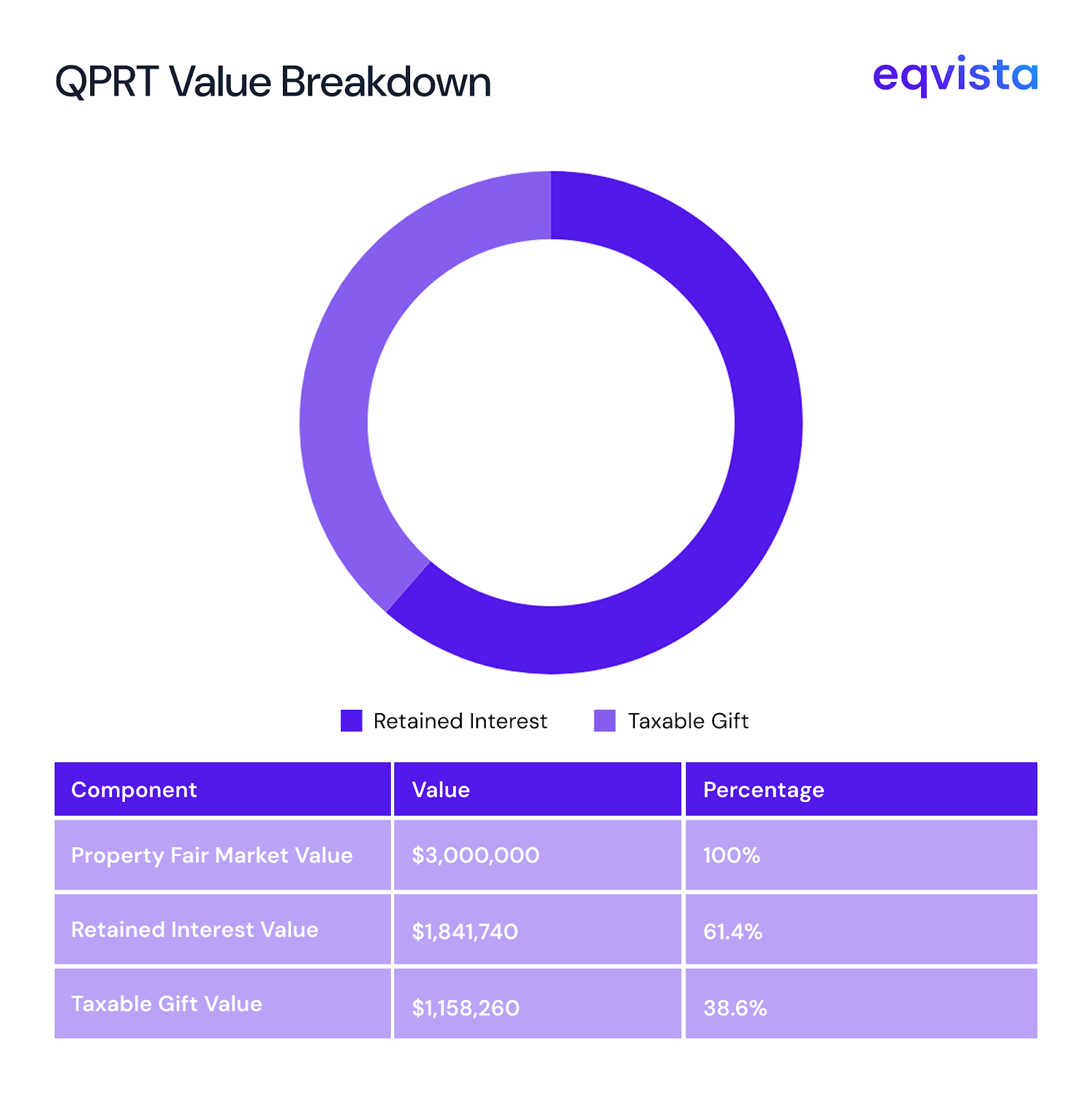

Qualified Personal Residence Trust (QPRTs)

Qualified Personal Residence Trusts (QPRTs) allow you to minimize the estate tax on residential property transfer. Transfers of properties placed in such trusts are taxed at a value lower than their fair market value (FMV) thereby reducing the amount of gift tax incurred.

In such trusts, the grantor would retain an interest in the property for a specified period. In this period, the grantor can continue living at the property. Once the grantor’s retained interest period is over, the property is transferred to the beneficiary.

Let us explore this with an example. Suppose your home is worth $3 million and you placed it in a QPRT with a term of 10 years. We also know that the present (June 2025) Section 7520 interest rate is 5%.

So, the value of your retained interest would be = Property’s fair market value (FMV)(1+Section 7520 interest rate)Number of years

= $3 million(1+5%)10

= $1,841,740

As a result, the transfer value would be = Property’s FMV – Value of retained interest

= $3,000,000 – $1,841,740

= $1,158,260

Let us calculate the tax savings achieved through the QPRT.

| Particulars | Transfer through QPRT | Direct transfer |

|---|---|---|

| Property value | $3,000,000 | $3,000,000 |

| Retained interest | $1,841,740 | $0 |

| Transfer value | $1,158,260 | $3,000,000 |

| Tax rate | 40% | |

| Tax liability | $463,304 | $1,200,000 |

| Tax savings unlocked through QPRT | $736,696 | |

Note: For the sake of simplicity, we have assumed a flat tax rate of 40%. In reality, you must calculate the tax liability as per the estate tax brackets.

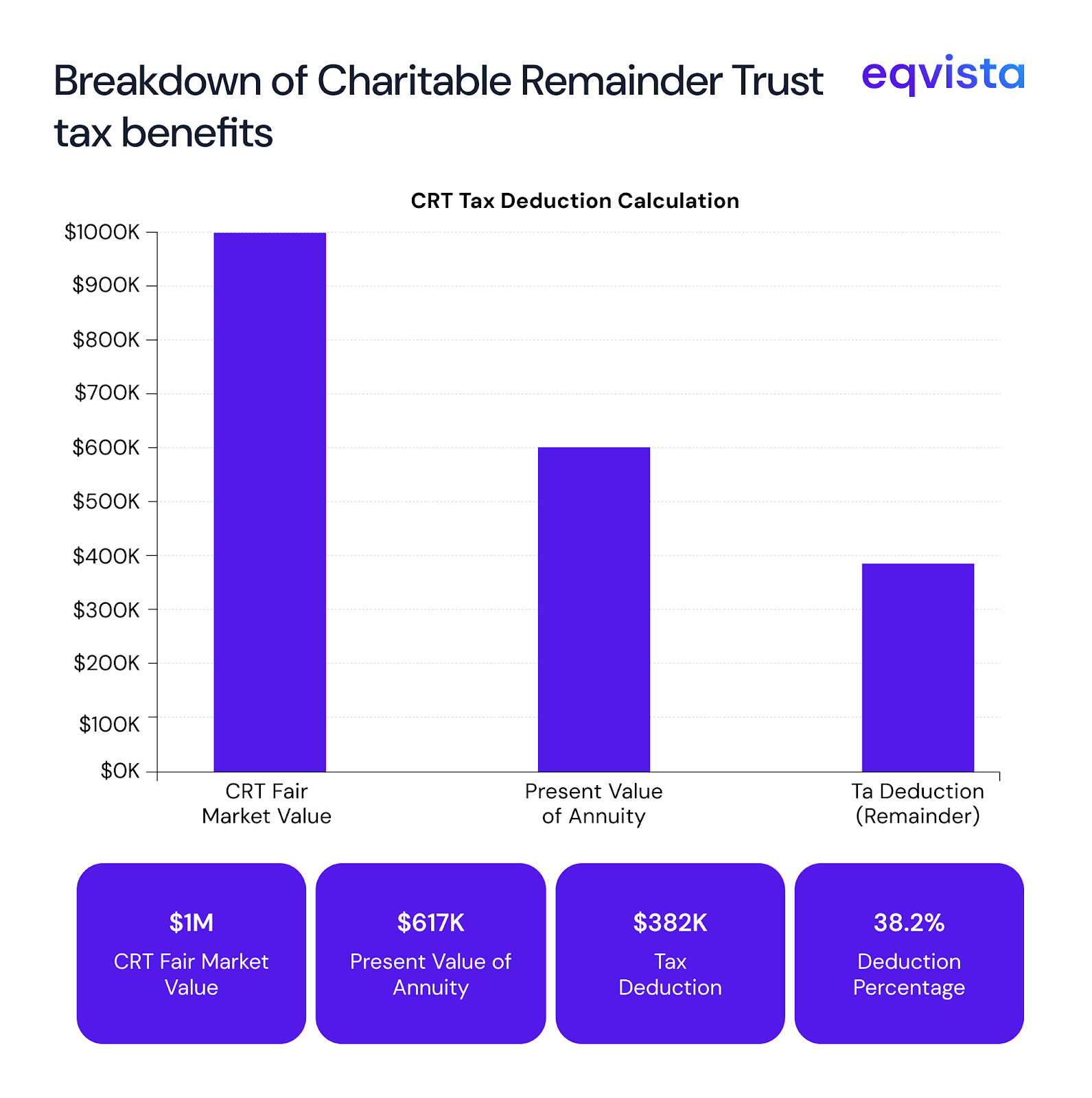

Charitable Remainder Trusts (CRTs)

Charitable remainder trusts (CRTs) pay a certain income to the grantor or other beneficiaries for a fixed period after which the remainder is transferred to a charity or charities, chosen by the grantor. A key benefit of CRTs is the immediate tax deduction they unlock for grantors. These tax deductions are equal to the present value of the remainder, i.e., contributions made to charities.

You could lose these tax benefits if the remainder’s actuarial value is less than 10% of the value of all assets in the CRT on the funding date.

Tax deduction calculation example

Suppose your CRT’s fair market value is $1 million, and it pays an annuity of $80,000 for 10 years. To find the present value of the remainder, we need to subtract the present value of the annuity from the fair market value.

We can find the present value of the annuity by applying the present value factor in the IRS’s actuarial table for an interest rate of 5% (the Section 7520 interest rate) and a term of 10 years.

So, the present value of the annuity is = Annuity × Present value factor

= $80,000 × 7.7217

= $617,736

Thus, the tax deduction = Present value of the remainder

= CRT’s fair market value – Present value of annuity

= $1,000,000 − $617,736

= $382,264

Since the present value of the remainder is greater than 10% of the CRT funding date valuation (i.e., $100,000), the tax deductions are valid.

Intentionally Defective Grantor Trusts (IDGTs)

You can set up an intentionally defective grant trust (IDGT) with a seed gift that is at least 10% of the value of assets you wish to transfer to your beneficiaries. Then, you can sell the remaining assets to the IDGT for a promissory note equal to the fair market value of the assets. Over the IDGT’s term, you will receive principal and interest payments from the IDGT.

During the IDGT’s term, as the grantor, you must pay the tax on the income generated by its assets. When the note is repaid, the trust continues to hold the remaining assets, which can ultimately pass to the beneficiaries without triggering additional gift or estate tax.

Although asset growth inside the IDGT is not taxed immediately, beneficiaries will owe capital gains tax upon sale, based on the grantor’s original cost basis.

Fully leveraging these tax benefits requires accurate valuations. Firstly, the promissory note’s value must be equal to the FMV of the assets sold. Secondly, to avoid triggering gift or estate taxes, the value of the seed gift must not exceed your available lifetime gift and estate tax exemption.

Eqvista- Unlocking tax savings with accuracy!

Trusts can be a powerful means for minimizing and even making ineffective the tax liabilities in succession. However, the actual tax savings depends on two critical factors: proper trust structuring and accurate asset valuation. Eqvista’s seasoned valuation analysts specialize in the latter, i.e., delivering accurate, defensible, and data-backed valuation reports. Contact us to know more!