Trust-based estate planning remains one of the most effective tools for protecting wealth, minimizing tax liability, and transferring assets to future generations. Its success often hinges on a critical factor: accurate asset valuation. Although recent legislation has made the current federal estate and gift tax exemption of $15 million per person permanent, many families are still turning to advanced planning strategies to lock in today’s favorable tax landscape.

This article explores five widely used trust structures and explains why professional, third-party appraisals are essential when valuing trust-held assets.

Benefits of third-party appraisals for Trust Asset Valuation

Appraisals from third-party valuation experts can help you tackle trust valuation complexities in the following manner:

Knowledge of IRS valuation guidelines

The IRS has established various valuation guidelines to prevent bad actors from unethically reducing their tax liabilities. These valuation guidelines are built in response to past income tax fraud cases and tax laws. Since a trust valuation can have numerous types of assets, it is extremely challenging for a single person to know all guidelines. Instead, you should rely on third-party valuation service providers whose teams include specialists for each type of asset valuation.

Timely appraisals

As per the Internal Revenue Code (IRC), a trust’s valuation must be declared within 9 months of the settlor’s demise, with a possible 6-month extension. While these filing deadlines may seem adequate, trust valuations can be incredibly complex, and finalizing estate tax strategies can be time-consuming. Hence, timely and accurate trust valuations from professional analysts can prove vital for tax compliance and avoiding heightened IRS scrutiny.

Informed decision-making

You need to make the right choice from numerous trust structures to transfer your assets in a tax-efficient manner. Making these comparisons might require numerous trust asset valuations that can only be provided by a professional third-party appraiser.

Unbiased perspective

When someone values their own assets, they are likely to make unrealistic assumptions based on whether these assets have delivered on their expectations or not in the past. If an asset has consistently delivered returns, you are likely to overvalue it. The opposite is also true.

In contrast, a third-party appraiser is likely to deliver a defensible valuation report free of any unrealistic assumptions born out of emotional attachment or similar irrational emotional factors.

Trust asset valuation complexities in commonly used trust structures

Here we will discuss five kinds of trusts frequently used for tax-efficient successions and highlight the valuation challenges involved in maximizing their benefits.

Grantor Retained Annuity Trusts (GRATs)

GRATs are primarily used to transfer assets at a lower value and thus, reduce the gift tax liability. GRATs are required to earn at least as much interest as the rates set by the Internal Revenue Service (IRS).

There are three instances when you will need valuations if you establish a GRAT. Firstly, you must transfer the assets at the fair market value on the gift date. Secondly, you must periodically review whether your GRAT can earn the required interest rate in time. Thirdly, if you expect to miss the required interest rate, you must substitute assets of equivalent value.

While the valuation requirement in the first instance (formation of the GRAT) is quite straightforward, we cannot say the same for the other two instances. You must assess whether your GRAT can pay out the required annuity or not. Then, you must find a replacement asset that can be expected to make up for the underperforming asset in time.

Qualified Personal Residence Trust (QPRTs)

QPRTs allow you to transfer your primary residence at a reduced valuation after living at said residence for the trust’s term. The retained interest is calculated as the present value of your right to live at said residence for the term. The present value is calculated using the Section 7520 interest rate for the month of valuation.

So, essentially, two kinds of valuations are required in the case of QPRTs. Firstly, you must calculate the fair market value of your primary residence. Secondly, you must apply the retained interest formula to the primary residence’s fair market value. Then, you must subtract the retained interest from the primary residence’s fair market value to arrive at the transfer value.

When valuing your residence, you must meticulously record the legal property description, ownership history, rental history, outlook of the property, general economic outlook, valuation date, and various other details.

Charitable Remainder Trusts (CRTs)

CRTs can help you unlock tax deductions equal to the contributions made to charitable entities. In these trusts, grantors and/or other non-charitable beneficiaries receive an income for the term and can claim tax deductions equal to the present value of the eventual contributions to charities.

However, these tax benefits cannot be claimed if the actuarial value of charitable contributions is less than 10% of the CRT on the funding date.

The actuarial value of the charitable contributions must be calculated using the Section 7520 interest rate. Actuarial value calculations can be slightly more complex than simple present value calculations. Here, you must apply the discounting rate provided by the IRS for the interest rate, term, and valuation factor.

Charitable lead trust (CLTs)

CLTs are similar to CRTs in the fact that CLTs, too, make distributions to charitable and non-charitable beneficiaries. The only difference is when these distributions are made. In CLTs, the annual payout is distributed to charities, while the remainder at the end of the term is distributed to non-charitable beneficiaries.

CLTs also provide an immediate tax deduction benefit equal to the present value of all charitable contributions. If the CLT is a grantor trust, the grantor can make the tax deduction, subject to certain limitations. In this case, the grantor must pay taxes on the CLT’s investment income.

On the other hand, if the CLT is a non-grantor trust, it can make the tax deductions without any limitations. Here, the trust must pay taxes on the investment income.

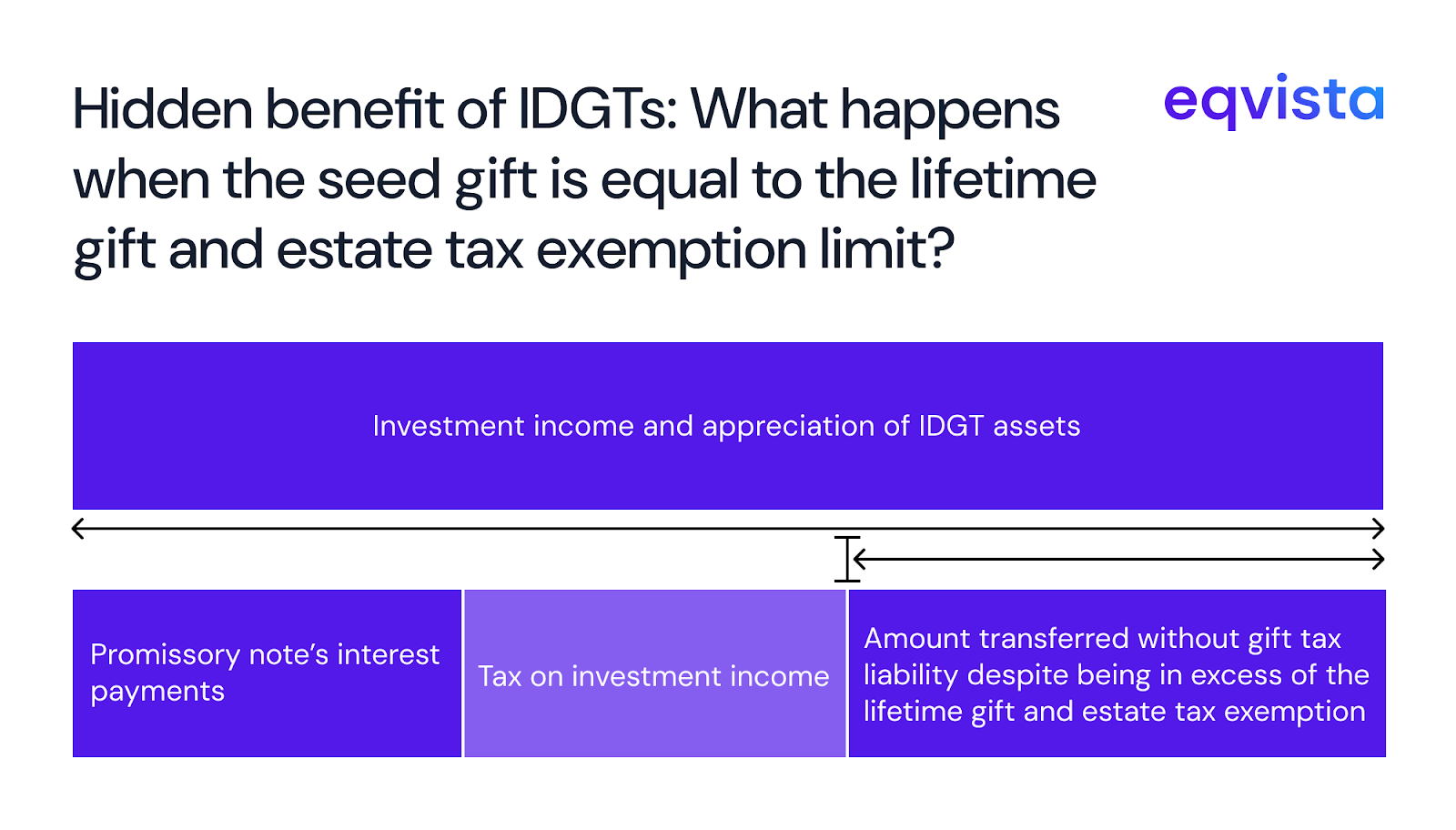

Intentionally Defective Grantor Trusts (IDGTs)

You can use an intentionally defective grantor trust (IDGT) to transfer assets on a future date without taxation on the appreciation of said assets. To unlock these benefits, you must ensure that the IDGT was set up with a seed gift that is at least 10% of the assets you intend to transfer. Then, you must sell the remaining assets to the IDGT in exchange for a promissory note.

Suppose the seed gift was equal to your lifetime gift and estate tax exemption limit. Also, assume that the remaining assets were valued at 9 times the seed gift. What happens if the trust’s post-tax investment income is greater than the interest on the promissory note? Then, you would have transferred assets worth much more than your lifetime gift and estate tax exemption limit without triggering gift tax liability.

Whether you can unlock this tax benefit depends on the following valuation-related aspects:

Was your seed gift 1/10th of the total intended gift?

Answering this question requires an IRS-compliant valuation of all assets slated to be transferred.

Did your post-tax investment income outpace the promissory note’s interest payments?

You must estimate your overall income tax liabilities over the trust’s term, estimate the investment income, and make valuation projections for all assets .

If your income and valuation projections suggest that the answer to both these questions is yes, then, you should utilize IDGTs for estate planning.

Summary Table: Comparing Trust Types

| GRAT | |

| QPRT | |

| CRT | Must calculate the present value of the charitable remainder using the Section 7520 rate. Actuarial calculations are needed to ensure the charitable portion is at least 10% of value. Selecting the correct IRS actuarial table and discount rate is critical and can be challenging. |

| CLT | |

| IDGT |

Understanding the Section 7520 interest rate

Section 7520 Rate is crucial in trust asset valuation because it determines the present value of future interests (like annuities, life estates, and remainder interests) for federal gift and estate tax purposes, ensuring standardized and IRS-compliant valuations.

A higher 7520 rate lowers the present value of future interests, often reducing taxable gifts but increasing the value of current income interests. A lower 7520 rate does the opposite, raising the present value of future interests and potentially increasing gift tax exposure.

Estate planning strategies (like GRATs, CLTs, and QPRTs) rely on the 7520 rate to maximize tax efficiency and wealth transfer opportunities.

Note: Knowing the Section 7520 Rate helps ensure accurate, defensible trust valuations and optimizes estate and gift tax planning

Eqvista- Accurately unlocking tax savings!

With the passage of the One Big Beautiful Bill (OBBB) Act, you no longer need to rush your estate planning. The lifetime gift and estate tax exemption limit is now set to increase to $15 million in 2026 and will be adjusted for inflation annually.

Eqvista is the perfect partner to help you fully capitalize on these favorable conditions. Under the guidance of a NACVA-certified valuation analyst, we have assembled a team of experts. Every month, we are entrusted with the valuation of client assets worth $2 billion.

We have a spotless track record of delivering defensible valuation reports with unprecedented agility. Contact us to learn more about our services!

Important Note: This article provides general information only and should not be considered legal, tax, or investment advice. Estate planning strategies involve complex tax and legal considerations that vary based on circumstances. Always consult with tax professionals, and valuation experts before implementing any strategy.