Qualified Small Business Stock (QSBS): What Is It and Why Does It Matter?

Maximize QSBS tax exemptions and learn how expert attestation helps founders and investors reduce capital gains.

Last Updated: May, 2026

In the US, the total capital gains tax can go as high as 50.3% in states such as California. This can significantly erode the earnings of investors and discourage investments into small businesses despite potential multifold returns.

Such problems have been dealt with through the provision of the Qualified Small Business Stock (QSBS) tax benefits. According to section 1202, individuals who own such stocks for than five years can exempt themselves from taxes to the extent of $10 million or ten times their adjusted basis of ownership in the QSBS stock.

For stock issued after July 4, 2025, under the One Big Beautiful Bill Act (OBBBA), this cap increases to $15 million or 10 times the adjusted basis, whichever is greater, with the $15 million limit indexed for inflation beginning January 1, 2027. However, you must comply with several requirements to qualify for these tax benefits.

QSBS offers several tax benefits to investors in early-stage startups and small businesses, allowing them to exclude all capital gains on their investments. This article explains what QSBS is, how businesses and investors can qualify for these benefits, and strategies to maximize gains while avoiding pitfalls.

Key Takeaways

- Ensure accurate and timely QSBS attestations from trusted valuation experts to support your claims.

- Regularly review your company’s asset composition to maintain QSBS tax eligibility.

- Consult tax professionals to integrate QSBS strategies with your overall investment or business exit plan.

What is Qualified Small Business Stock (QSBS)?

Qualified Small Business stock(QSBS) is a special tax provision under the Internal Revenue Code under Section 1202.

It gives an attractive advantage by allowing investors to exclude tax on capital gains – up to 100 percent of their gains if the stock is held for at least five years – capped at either $15 million or ten times their investment basis, whichever is higher. To qualify for these benefits, the investors must hold their QSBS investments for at least 5 years.

If your holding period is 4 years, the available tax exclusion reduces to 75% and when it is 3 years, the available tax exclusion drops further to 50%. Any holding periods shorter than 3 years do not qualify for QSBS benefits.

One of the requirements to be considered as a QSB is that one needs to have a gross asset worth of less than $75 million both before and after the QSBS has been issued, where the QSBS stock issuance will take place on or after July 5, 2025, after the passage of the OBBBA; the previous threshold was $50 million. In addition, you cannot purchase QSBS stocks from shareholders to reap those tax benefits. You need to obtain those QSBS from the corporation in return for some consideration.

To qualify, the stock must be issued directly by a domestic C-corporation meeting specific asset, business activity, and holding requirements.

QSBS Eligibility Requirements

A business must meet certain key requirements about asset value and use, industry of operation, and corporate structure to qualify for QSBS treatment. These requirements are listed below:

- The company must be a domestic C corporation.

- The stock must be issued at original issuance in exchange for money, property, or services.

- The company must satisfy the gross assets test at the time the stock is issued.

- The company must operate in a qualifying active business.

- The company must avoid disqualified industries, such as certain service, financial, and investment businesses.

- The stockholder must generally hold the stock for more than five years to claim the full exclusion.

- Certain redemptions, restructurings, or business changes can affect QSBS treatment.

For founders, QSBS is a game of foresight. The diligent paperwork you complete in your earliest, leanest days is what ultimately secures your multi-million-dollar tax exemption years down the line. – Brayton Johnson, COO & Head of Revenue, Eqvista

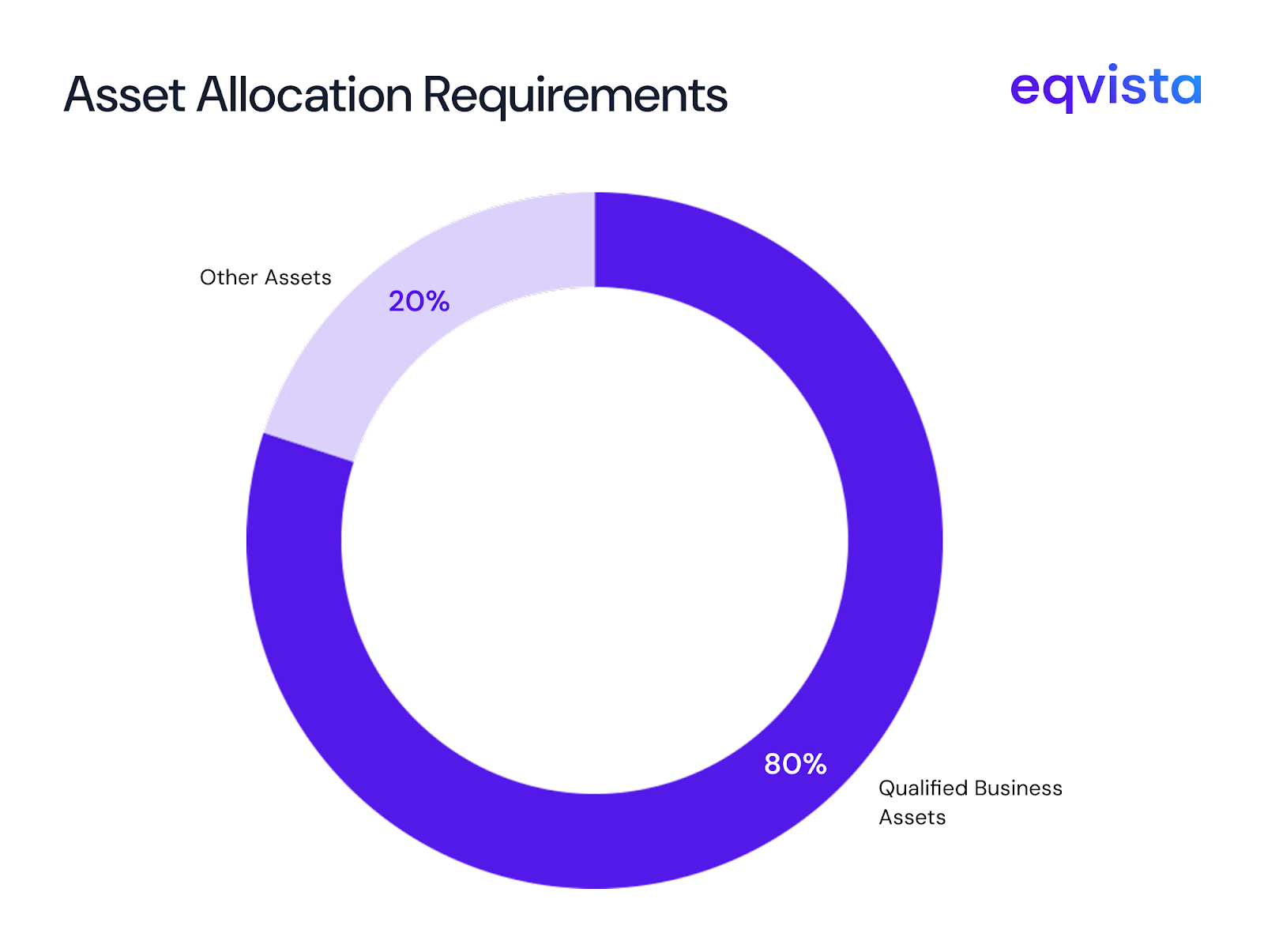

QSBS Asset-related Eligibility requirements

- A business’s gross assets must be less than $75 million (before and immediately after investment) to qualify for QSBS treatment.

- At least 80% of these assets must be actively engaged in a qualified trade or business, i.e., in an industry not explicitly disqualified under Section 1202.

Securities holding-related requirement

To maintain QSBS status, a company must:

- Limit its holdings of stock and securities of non-subsidiary entities to less than 10% of its net assets.

- Limit real estate holdings in disqualified businesses or trades to under 10% of total assets.

Any time these thresholds are exceeded does not count toward the required five-year holding period.

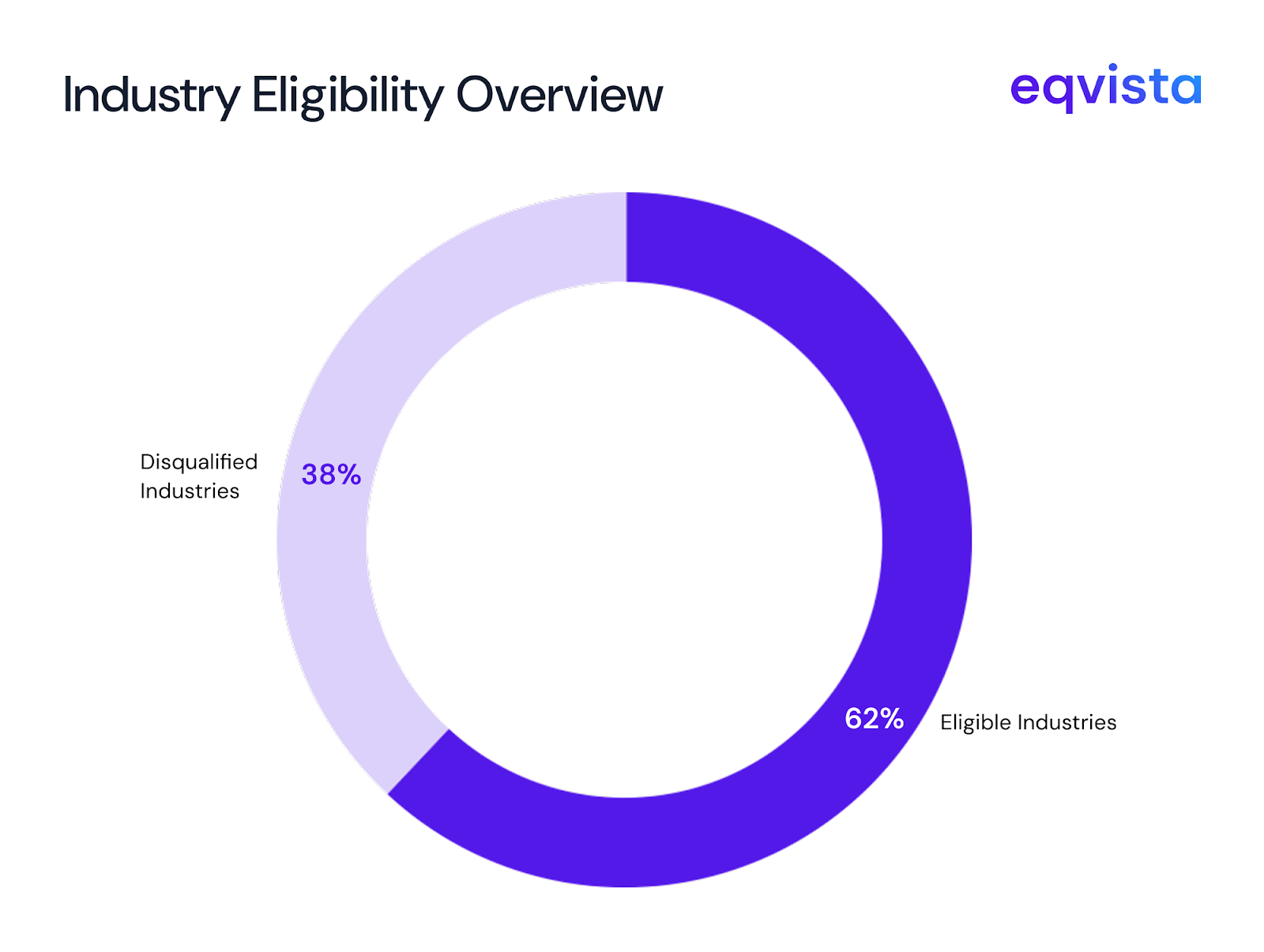

Disqualified industries

A business that does not operate in the following industries can qualify for QSBS treatment:

- Professional services such as actuarial science, consulting, and law

- Athletics and performing arts

- Banking, financing, insurance, and other related industries

- Agriculture

- Businesses involved in extracting products for which deductions are allowed under Section 613 or Section 613A

- Hospitality

- Businesses whose principal asset is the skill of one or more employees

Strategies for Maximizing QSBS Tax Benefits

To qualify for the QSBS tax exclusion, investors must acquire stock directly from the company and hold it for the required five-year period, ensuring they maximize the tax advantages available. The core advantage of QSBS lies in its ability to reduce or eliminate the capital gains tax liability on profits from the sale of stock, as long as investors meet the holding period and other qualifying criteria. To maximize your gains from QSBS treatment, founders and investors must apply the following strategies.

QSBS Strategies For Founders

Start as a C-Corporation from day one to avoid resetting QSBS eligibility. Issue founder shares at formation when valuation is lowest and file 83(b) elections immediately. Monitor gross assets carefully to stay under $75 million by timing fundraising strategically and using debt financing when approaching limits. Structure employee equity as restricted stock grants rather than options and ensure all recipients file timely 83(b) elections.

The QSBS is sustained if the business activities are maintained at 80% of the company’s total asset value, and it excludes any service that is not directly involved in the operations such as consultation or hotel. One way to get more exclusions is to issue shares to other family members, because each person would get an exemption limit of $15 million as of July 4, 2025 – previously $10 million based on shares issued after this date per issuer.

QSBS Strategies for Investors

Focus exclusively on primary market investments in original company issuances, never secondary purchases. Target seed and early-stage rounds when valuations are lower for maximum appreciation potential.

Verify each company’s QSBS qualification including C-Corp structure, sub-$75 million assets, and qualifying business activities.

Ensure that you build a portfolio consisting of more than one qualifying business since each is capable of offering an exclusion chance of up to $15 million if stocks have been sold after July 4, 2025, or $10 million if before then.

Carefully track the holding period requirements for the mandated 5-year minimum requirement. Look at how family members can invest to increase gains, as each one gets his/her own $15 million per issuer cap if the shares are acquired after July 4, 2025, or the $10 million per issuer cap if prior to that date. Use section 1045 rollover provisions to postpone gain recognition by reinvesting proceeds in newly acquired QSBS within 60 days. Never invest through partnerships or funds.

The shortest period of time to meet the criteria of any QSBS tax exclusion is three years, which qualifies for a 50% exclusion. Four years results in a 75% exclusion, whereas a complete 100% exclusion can only be enjoyed after a period of five years. Please note that any period during which the requirement of assets or holding period is not fulfilled will not count towards the required time period.

Example: Potential Tax Savings With QSBS

| Investment Basis | Gains | Available Exclusion (Post-July 4, 2025) | Exclusion Rule Applied | Taxable Gains | Tax Savings (50.3%) |

|---|---|---|---|---|---|

| $1M | $15M | $15M | $15M cap (equals gain) | $0 | $7.50M |

| $500K | $7M | $7M | Gain < $15M cap; exclusion = actual gain | $0 | $3.52M |

| $2M | $20M | $15M | $15M cap applies;10x adjusted basis=$20M | $5M | $7.54M |

What Is the QSBS Filing Process?

To claim QSBS benefits, investors must accurately report their capital gains on the relevant tax filings and demonstrate eligibility for the exclusion to minimize or defer capital gains tax.

For claiming the QSBS tax exclusion Investors must file:

- IRS Form 8949 and Schedule D for capital gains reporting

- Form 1045 to elect deferrals or rollovers if applicable

- Forms you may receive: Form 1099-B (from your broker, reporting sale proceeds), Form 1099-CAP (from the corporation, reporting acquisition changes), and Schedule K-1 (from a partnership or fund, reporting your share of income or loss)

- Forms you may need to file: Form 6251 (Alternative Minimum Tax) and Form 8960 (Net Investment Income Tax), both attached to your personal tax return as applicable

Furthermore, you must ensure that your portfolio companies get a QSBS attestation from a trusted valuation expert such as Eqvista.

Think of the QSBS tax exemption as a locked treasure chest. The attestation is the key. Our job is to hand that key to founders to unlock their millions. Shivank Agarwal, Senior Associate – Valuation and Advisory, Eqvista

Disqualification Triggers of QSBS

Failure to meet QSBS requirements may lead to disqualification, exposing investors to full capital gains tax on the accrued profits from their stock sales. You may not qualify for QSBS tax benefits in the following circumstances.

- Exceeding the $75 Million Asset Threshold – When you invest in a business with the intention of availing QSBS tax treatment, you must ensure that the business’s gross asset value does not exceed $75 million before and immediately after the investment is made. Otherwise, it would result in automatic disqualification.

- Business Model Changes – QSBS tax benefits are available only for companies whose 80% of assets are actively engaged in qualified businesses and trades.

- Improper Share Repurchases – Shares might lose their QSBS status if they were issued up to one year before repurchases exceeding a certain threshold or up to one year after such an event. This threshold is calculated as 5% of the aggregate value of all stock at the beginning of this 2-year period.

Furthermore, in the 4-year period starting 2 years before the issuance date, if the company redeemed stock from the investor or related persons, these stocks would not qualify as QSBS.

Improper Asset Management

As a founder, you must ensure that your real estate holdings engaged in non-qualified businesses and trade do not exceed 10% of total assets. Furthermore, you must also be careful not to hold stocks and securities of non-subsidiaries exceeding 10% of your net assets.

Summary Table of Common QSBS Disqualification Triggers

| Disqualification Trigger | Key Details |

|---|---|

| Asset Threshold | Exceeding $75M at issuance or immediately after |

| Business Qualification | Less than 80% of assets in qualified trades or businesses |

| Share Redemptions | Significant redemptions within one year before/after issuance (≥5% for general, ≥2% for related parties) |

| Excess Securities/Real Estate Holdings | Over 10% in non-subsidiaries securities or non-qualified real estate |

| Share Transfers | Failure to meet QSBS conditions on secondary transfers |

Careful planning around these triggers is essential to preserve QSBS eligibility and maximize tax benefits. Companies and investors should seek expert guidance to navigate these complex rules.

FAQs

Some common queries about QSBS are as follows:

What qualifies as QSBS?

Shares may qualify as QSBS if they were directly issued in exchange for money, services, and property other than shares by domestic C-corporations with gross assets of $75 million, 80% of which are engaged in qualified businesses.

What is the redemption rule for QSBS?

Redemptions exceeding a certain threshold or redemptions of stocks owned by the QSBS investor or related persons might result in disqualifications.

How do I claim QSBS?

To claim QSBS tax benefits, you may need to file Form 8949, Schedule D, Form 1045, Form 1099-B, Form 1099-CAP, Schedule K-1, Form 6251, and Form 8960.

What is the 10 times basis for QSBS?

For QSBS, the “10 times basis” rule means you can exclude gain up to 10 times your aggregate adjusted basis in the QSBS issued by that corporation during the tax year, subject to the overall per-issuer cap.

What Tax Benefits Does QSBS Provide?

- More than five years: The exclusion amount is equal to 100% of the gains; however, this is limited to $10 million or 10 times the taxpayer’s adjusted basis for the QSBS stock. This limit is increased to $15 million for corporations that were issued after July 4, 2025 under the OBBBA.

- Four years: Excludes 75% of the gain and follows the above cap.

- Three years: Excludes 50% of the gain and follows the above cap.

- Less than three years: There is no exclusion allowed.

How Can Founders Set Up Their Business for QSBS Benefits?

You must establish your business as a domestic C-corporation and be mindful of the requirements regarding asset value, asset use, and stock and securities holdings. You must also abide by the real estate holding use requirements.

How Can Investors Leverage QSBS in Their Investment Strategy?

Investors can leverage the QSBS strategy when they are seeking investment opportunities in early-stage startups. However, these companies are high-risk assets and investors must also diversify with less risky assets.

Can QSBS be rolled over?

Yes, capital gains can be deferred by reinvesting proceeds into new QSBS within 60 days under Section 1045, preserving the original holding period.

How long must I hold QSBS to qualify?

At least five years for maximum benefits; more, if holding period requirements are interrupted by disqualifying asset holdings.

What is the QSBS tax exclusion?

The QSBS tax exclusion allows investors to exclude from taxable income a substantial portion of the capital gains realized from the sale of qualified small business stock held for at least three years, subject to certain limits and requirements.

Eqvista – Unlocking tax savings through accuracy!

Meeting asset value and use requirements is the crux to unlocking QSBS tax benefits. Eqvista can help you surpass these hurdles through accurate QSBS attestations.

We can also help investors validate that the requirements regarding stocks and securities of non-subsidiaries and real estate use were met during the investment period. Contact us to learn more about our services!

Interested in issuing & managing shares?

If you want to start issuing and managing shares, Try out our Eqvista App, it is free and all online!