Qualification Criteria for Rule 701 Exemption

Rule 701 allows companies to issue equity compensation without registering the securities under the Securities Act.

Note: The Rule 701 feature is only available for premium account holders. Kindly upgrade your account to unlock this feature.

After selecting the securities, the aggregate sales price or amount of securities sold within a continuous 12-month period must meet one of the qualification criteria for generating the report.

Rule 701 exemption – Qualification criteria

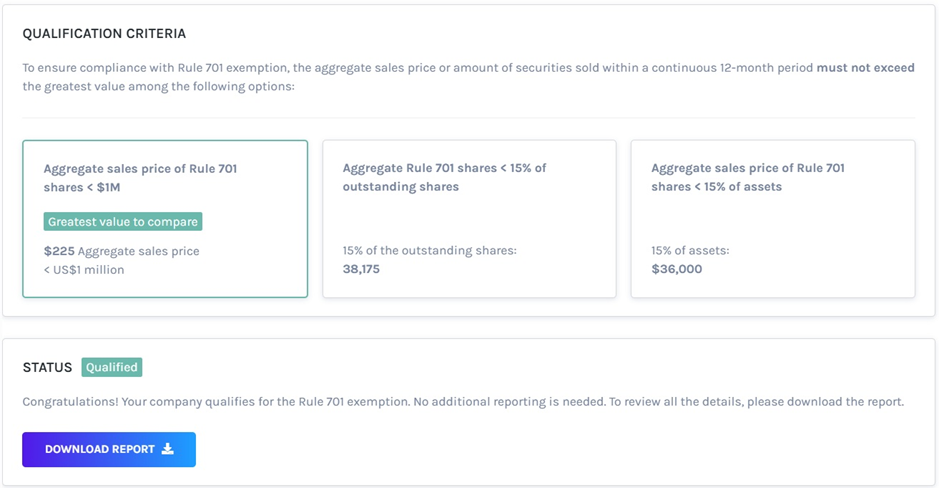

The aggregate sales price sold under Rule 701 is less than $1 million.

Let’s consider an example that shows in detail how the criterion “Pass” and “Fail”.

| Amount of Securities | 1000 |

|---|---|

| Price per Share | $0.05 |

| Sales Price (Amount of Securities * Price per Share) | $50 |

| Aggregate Sales Price | $225 |

| Aggregate Sales Price < $1 million | $225 < $1,000,000 Pass |

The system calculates the value of all 3 qualification criteria, finds the highest case, and applies that as the “Greatest Value to Compare”.

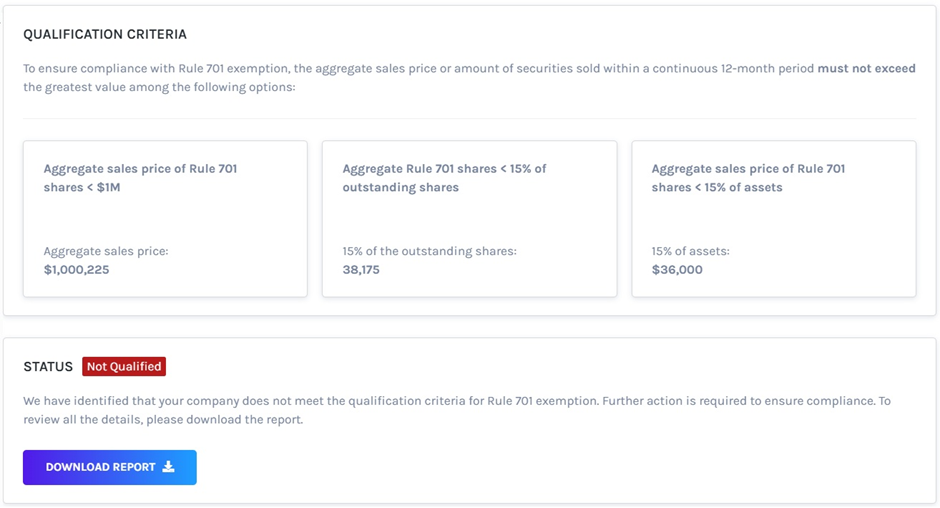

| Amount of Securities | 250,000 |

|---|---|

| Price per Share | $4 |

| Sales Price (Amount of Securities * Price per Share) | $1,000,000 |

| Aggregate Sales Price | $1,000,225 |

| Aggregate Sales Price < $1 million | $1,000,225 > $1,000,000 Fail |

When it “Fails” in this particular criterion, we still need to continue checking the other two criteria.

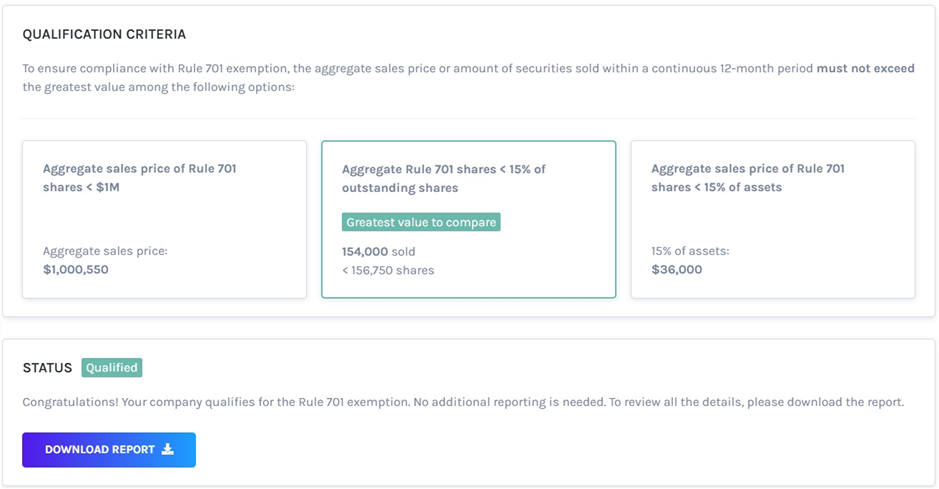

The aggregate securities sold under Rule 701 are less than 15% of outstanding shares

Here is an example that shows in detail how the criterion “Pass” and “Fail”.

| Aggregate Securities | 154,000 |

|---|---|

| Outstanding Shares | 1,045,000 |

| 15% of Outstanding Shares (0.15 * Outstanding Shares) | 156,750 |

| Aggregate Securities < 15% of Outstanding Shares | 154,000 < 156,750 Pass |

The system calculates the value of all 3 qualification criteria, finds the highest case, and applies that as the “Greatest Value to Compare”.

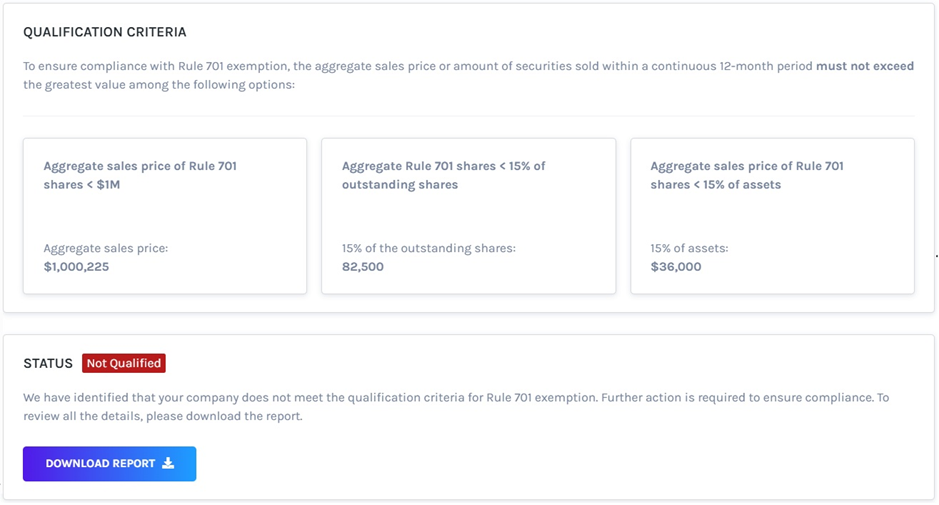

| Aggregate Securities | 154,000 |

|---|---|

| Outstanding Shares | 550,000 |

| 15% of Outstanding Shares (0.15 * Outstanding Shares) | 82,500 |

| Aggregate Securities < 15% of Outstanding Shares | 154,000 > 82,500 Fail |

When it “Fails” in this particular criterion, we still need to continue checking the other criteria.

The aggregate sales price sold under rule 701 is less than 15% of total assets

An example that shows in detail how the criterion “Pass” and “Fail”.

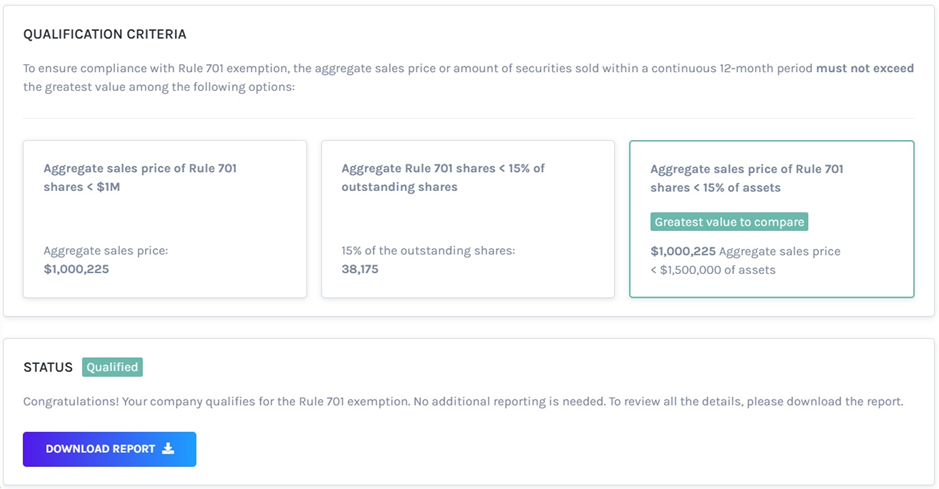

| Aggregate Sales Price | $1,000,225 |

|---|---|

| Total Assets | $10,000,000 |

| 15% of Total Assets (0.15 * Outstanding Shares) | $1,500,000 |

| Aggregate Securities < 15% of Total Assets | $1,000,225 < $1,500,000 Pass |

The system calculates the value of all 3 qualification criteria, finds the highest case, and applies that as the “Greatest Value to Compare”.

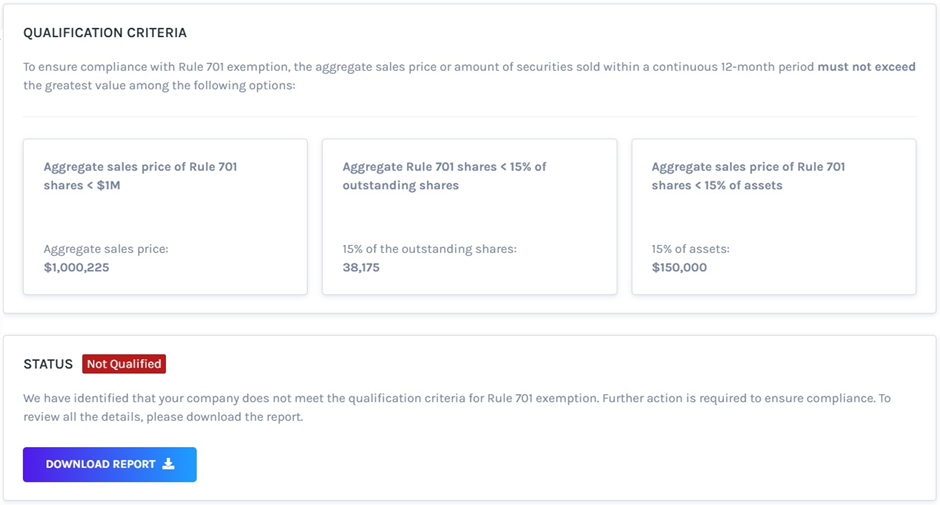

| Aggregate Sales Price | $1,000,225 |

|---|---|

| Total Assets | $1,000,000 |

| 15% of Total Assets (0.15 * Outstanding Shares) | $150,000 |

| Aggregate Securities < 15% of Total Assets | $1,000,225 > $150,000 Fail |

When it passes one of the criteria, the status shows the company is “Qualified” for Rule 701 exemption.

The report gets downloaded as an Excel sheet in your Downloads. To know more about the details of the downloaded report, check out our support article!

For more information on Eqvista, check out our support articles or contact us for any queries!